| TURKEY’S LEADING MOBILITY APP |

| About this Presentation This confidential presentation (this “Presentation”) is for informational purposes only to assist interested parties in making their own evaluation with respect to an investment in connection with a possible transaction (the “Business Combination”) involving Marti Technologies Inc.(“Marti” or the “Company”) and Galata Acquisition Corp.(“Galata” or “SPAC”), and for no other purpose. The information contained herein does not purport to be all-inclusive and none of Galata, the Company or their respective representatives or affiliates makes any representation or warranty, express or implied, as to the accuracy, completeness or reliability of the information contained in this Presentation. This Presentation and any oral statements made in connection with this Presentation do not constitute (i) a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the proposed Business Combination or (ii) an offer to sell, a solicitation of an offer to buy or a recommendation to purchase any securities. No such offering of securities shall be made except by means of a prospectus meeting the requirements of section 10 of the Securities Act of 1933, as amended (the “Securities Act”), or an exemption therefrom. You should not construe the contents of this Presentation as legal, tax, accounting, investment or other advice or a recommendation. You should consult your own counsel and tax and financial advisors as to legal and related matters concerning the matters described herein, and, by accepting this Presentation, you confirm that you are not relying upon the information contained herein to make any decision. The distribution of this Presentation may also be restricted by law and persons into whose possession this Presentation comes should inform themselves about, and observe, any such restrictions. The recipient acknowledges that it is (a) aware that the United States securities laws prohibit any person who has material, non-public information concerning a company from purchasing or selling securities of such company or from communicating such information to any other person under circumstances in which it is reasonably foreseeable that such person is likely to purchase or sell such securities, and (b) familiar with the Securities Exchange Act of 1934, as amended, and the rules and regulations promulgated thereunder (collectively, the "Exchange Act"), and that the recipient will neither use, nor cause any third party to use, this Presentation or any information contained herein in contravention of the Exchange Act, including, without limitation, Rule 10b-5 thereunder. This Presentation and information contained herein constitutes confidential information and is provided to you on the condition that you agree that you will hold it in strict confidence and not reproduce, disclose, forward or distribute it in whole or in part without the prior written consent of SPAC and the Company and is intended for the recipient hereof only. By accepting this Presentation, the recipient agrees (a) to maintain the confidentiality of all information that is contained in this Presentation and not already in the public domain and (b) to return or destroy all copies of this Presentation or portions thereof in its possession upon request. This Presentation is being distributed to selected recipients only and is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Neither this Presentation nor any part of it may be taken or transmitted into the United States or published, released, disclosed or distributed, directly or indirectly, in the United States, as that term is defined in the Securities Act, except to a limited number of qualified institutional buyers, as defined in Rule 144A under the Securities Act, or institutional “accredited investors” within the meaning of Regulation D under the Securities Act. Forward Looking Statements Certain statements in this Presentation may be considered forward-looking statements within the meaning of the U.S. federal securities laws with respect to the proposed Business Combination. Forward-looking statements generally relate to future events, such as the benefits of the Transaction or the anticipated timing of the Transaction, or SPAC or the Company’s future financial or operating performance. For example, statements regarding anticipated growth in the industry in which the Company operates and anticipated growth in demand for the Company’s products, projections of the Company’s future financial results, possible growth opportunities for the Company and other metrics are forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as “pro forma,” “may,” “should,” “could,” “might,” “plan,” “possible,” “project,” “strive,” “budget,” “forecast,” “expect,” “intend,” “will,” “estimate,” “anticipate,” “believe,” “predict,” “potential” and “continue” or the negatives of these terms or variations of them or similar terminology. Such forward-looking statements are subject to risks, uncertainties and other factors which could cause actual results to differ materially from those expressed or implied by such forward-looking statements. These forward-looking statements are based upon estimates and assumptions that, while considered reasonable by SPAC, the Company and their respective management, as the case may be, are inherently uncertain. Factors that may cause actual results to differ materially from current expectations include, but are not limited to: competition; the ability of the company to grow and manage growth, maintain relationships with consumers, suppliers and strategic partners and retain its management and key employees; costs related to the Business Combination; changes in applicable laws or regulations; the possibility that the Company may be adversely affected by other economic, business or competitive factors; the Company’s estimates of expenses and profitability; the evolution of the markets in which the Company competes; the ability of the Company to implement its strategic initiatives and continue to innovate its existing products; the ability of the Company to defend its intellectual property; and the impact of the COVID-19 pandemic on the Company’s business. Nothing in this Presentation should be regarded as a representation by any person that the forward-looking statements set forth herein will be achieved or that any of the contemplated results of such forward-looking statements will be achieved. You should not place undue reliance on forward-looking statements, which speak only as of the date they are made. Neither SPAC nor the Company undertakes any duty to update or revise these forward-looking statements. You should consult the risk factors included in this Presentation and SPAC’s public filings with the SEC, including the “Risk Factors” section in the registration statement on Form F-4 and the proxy statement included therein (the “Registration Statement”) that SPAC intends to file relating to the proposed Transaction and the “Risk Factors” section of other documents that SPAC files with the SEC from time to time, for additional information regarding risks and uncertainties related to the potential Transaction and which could cause actual future events to differ materially from the forward-looking statements in this Presentation. Forward-looking statements speak only as of the date they are made. Readers are cautioned not to put undue reliance on forward-looking statements, and SPAC and Marti assume no obligation and do not intend to update or revise these forward-looking statements, whether as a result of new information, future events or otherwise. Disclaimers 2 |

| Use of Projections This Presentation contains financial forecasts for the Company with respect to certain financial results for the Company’s fiscal years 2022 through 2023. The Company’s independent auditors have not audited, studied, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this Presentation, and accordingly, they did not express an opinion or provide any other form of assurance with respect thereto for the purpose of this Presentation. These projections are forward-looking statements and should not be relied upon as being necessarily indicative of future results. In this Presentation, certain of the above-mentioned projected information has been provided for purposes of providing comparisons with historical data. The assumptions and estimates underlying the prospective financial information are inherently uncertain and are subject to a wide variety of significant business, economic, competitive and other risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information. Accordingly, there can be no assurance that the prospective results are indicative of the future performance of the Company or that actual results will not differ materially from those presented in the prospective financial information. Inclusion of the prospective financial information in this Presentation should not be regarded as a representation by any person that the results contained in the prospective financial information will be achieved. The performance projections and estimates are subject to the ongoing COVID-19 pandemic, and have the potential to be revised to take into account further adverse effects of the COVID-19 pandemic on the future performance of SPAC and Marti. Projected financial results and estimates are based on an assumption that public health, economic, market and other conditions will improve; however, there can be no assurance that such conditions will improve within the time period or to the extent estimated by SPAC or Marti. The full impact of the COVID-19 pandemic on future performance is particularly uncertain and difficult to predict; therefore actual results may vary materially and adversely from the projections included herein. Financial Information; Non-GAAP Measures The financial information and data contained in this Presentation is unaudited and does not conform to Regulation S-X promulgated under the Securities Act. Such information and data may not be included in, may be adjusted in or may be presented differently in, the registration statement on Form S-4 to be filed relating to the Business Combination and the proxy statement/prospectus contained therein. This Presentation also includes certain financial measures not presented in accordance with generally accepted accounting principles of the United States (“GAAP”) including, but not limited to, Adjusted EBITDA and certain ratios and other metrics derived therefrom. The Company defines Adjusted EBITDA as net income (loss) plus non-operating income (loss), depreciation and amortization, net interest expense, income taxes, stock-based compensation and transaction costs. These non-GAAP financial measures are not measures of financial performance in accordance with GAAP and may exclude items that are significant in understanding and assessing the Company’s financial results. Therefore, these measures should not be considered in isolation or as an alternative to net income, cash flows from operations or other measures of profitability, liquidity or performance under GAAP. You should be aware that the Company’s presentation of these measures may not be comparable to similarly-titled measures used by other companies. The Company believes these non-GAAP measures of financial results provide useful information for management and investors regarding certain financial and business trends relating to the Company’s financial condition and results of operations. The Company believes the use of these non-GAAP financial measures provides an additional tool for investors to use in evaluating ongoing operating results and trends and in comparing the Company’s financial measures with other similar companies, many of which present similar non-GAAP financial measures to investors. These non-GAAP financial measures are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non-GAAP financial measures. This Presentation also includes certain projections of non-GAAP financial measures. Due to the high variability and difficulty in making accurate forecasts and projections of some of the information excluded from these projected measures, together with some of the excluded information not being ascertainable or accessible, the Company is unable to quantify certain amounts that would be required to be included in the most directly comparable GAAP financial measures without unreasonable effort. Consequently, no disclosure of estimated comparable GAAP measures is included and no reconciliation of the forward-looking non-GAAP financial measures is included. Industry and Market Data In this Presentation, SPAC and the Company rely on and refer to certain information and statistics obtained from third-party sources which SPAC and the Company believe to be reliable. While SPAC and the Company believe such third-party information is reliable, there can be no assurance as to the accuracy or completeness of the indicated information, and the Company has not independently verified the accuracy or completeness of any such information. Trademarks This Presentation contains trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective owners. The Company’s use thereof does not imply an affiliation with, or endorsement by, the owners of such trademarks, service marks, trade names and copyrights. Solely for convenience, some of the trademarks, service marks, trade names and copyrights referred to in this Presentation may be listed without the TM, SM © or ® symbols, but the Company will assert, to the fullest extent under applicable law, the rights of the applicable owners to these trademarks, service marks, trade names and copyrights. There is no guarantee that either SPAC or the Company will work, or continue to work, with any of the firms or businesses whose logos are included herein in the future. Disclaimers (cont’d) 3 |

| Marti is an excellent match for Galata Profitable and scalable unit economics reinforcing a discernible competitive advantage Favorable regulatory structure encouraging growth and opportunities for data-driven digital distribution Further industry consolidation opportunities Low penetration rates and favorable demographics Annual market growth significantly in excess of inflation 4 Galata has deep expertise and extensive experience in Turkey ● 35+ years of executive and management experience in Turkey ● Senior Advisor to The Blackstone Group ● Former CEO of Yapi Kredi Group, one of the leading financial groups in Turkey Kemal Kaya CEO ● 20+ years of experience in Turkey ● CIO of Callaway Capital Management ● Turkish speaker Daniel Freifeld President ● 13+ years of investment experience ● Portfolio Manager at Callaway Capital Management ● Former Senior Analyst at Southpaw Asset Management Michael Tanzer CFO |

| 5 ● Marti is Turkey’s leading mobility provider, operating a fleet of e-scooters, e-bikes, and e-mopeds, serviced by proprietary software systems and IoT infrastructure ● Marti has achieved strong growth and best- in-class unit profitability1 ● As the #1 mobility app on the iOS & Android stores in Turkey, Marti seeks to become Turkey’s first mobility super app by expanding into other attractive adjacencies, leveraging its growing and loyal customer base Transaction summary ● Galata is a NYSE-listed special purpose acquisition company which proposes to close a merger with Marti in Q4 2022 ● Pro-forma enterprise value of c.$532 million and equity value of c.$630 million o Implied pro forma enterprise value of 4.2x 2023FD (Fully Deployed2) net revenue of c.$125 million and 9.7x 2023FD (Fully Deployed2) EBITDA of c.$55 million o $57.5 million convertible note PIPE commitments plus assumed incremental PIPE commitments of up to $92.5 million to be raised post-announcement will fund future growth ● Marti shareholders are rolling 100% of their equity and are expected to own c.50%3 of the Company at close About Marti Transaction overview ● Background checks on management and shareholders ● Engagement of leading global audit and accounting firm for financial due diligence ● Engagement of international and local counsel for legal due diligence ● Engagement of the world’s leading business consultancy for comprehensive commercial due diligence ● Comprehensive evaluation of competitors and comparative transactions ● Independent analysis of current market share, unit economics, and regulatory regime Due diligence conducted by Galata Source: Company information, Helbiz and Bird investor presentations and SEC filings. Note: 1. In FY2021, Marti had a positive (+1%) EBITDA margin vs Bird’s (-33%) and Helbiz’s (-409%) significantly negative EBITDA margins. 2. FD refers to Fully Deployed figures that Marti would be expected to achieve in 2023 if only the proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement were to be deployed towards purchasing E-Scooters, E-Mopeds and E-Bikes immediately upon receipt. 3. Based on the Pro-Forma Diluted Ownership laid out on the Detailed transaction overview slide. |

| Marti Overview |

| We believe… 7 Transportation is the number one issue in emerging market megacities Everything on wheels will be electric… … and everything electric will be shareable Source: Company information. |

| Levan Yakut Chief Vehicle Officer Leadership team… 8 Management team cumulatively has c.85 years of experience across technology, telecommunications, finance, and consulting industries Cankut Durgun Cofounder, President Sena Öktem Cofounder, Deputy CEO İrem Bilgic Chief Operating Officer Alper Öktem Founder, CEO Eyal Enriquez Chief Strategy Officer Erdem Selim Chief Financial Officer Source: Company information. |

| …backed by investors with strong knowhow of Turkey and mobility Marti’s diverse investor base includes the leading mobility funds in the Valley and MENAT region, the largest private equity fund in Turkey and the largest provider of international finance to Turkey 9 Leading early stage VC and mobility investor in MENAT Silicon Valley-based early stage VC, dedicated to global mobility The largest private equity primarily focusing on investments in Turkey San Francisco-based debt financing provider to high growth technology companies UAE-based global venture capital investor Leading provider of international finance to Turkey’s public sector Source: Company information. |

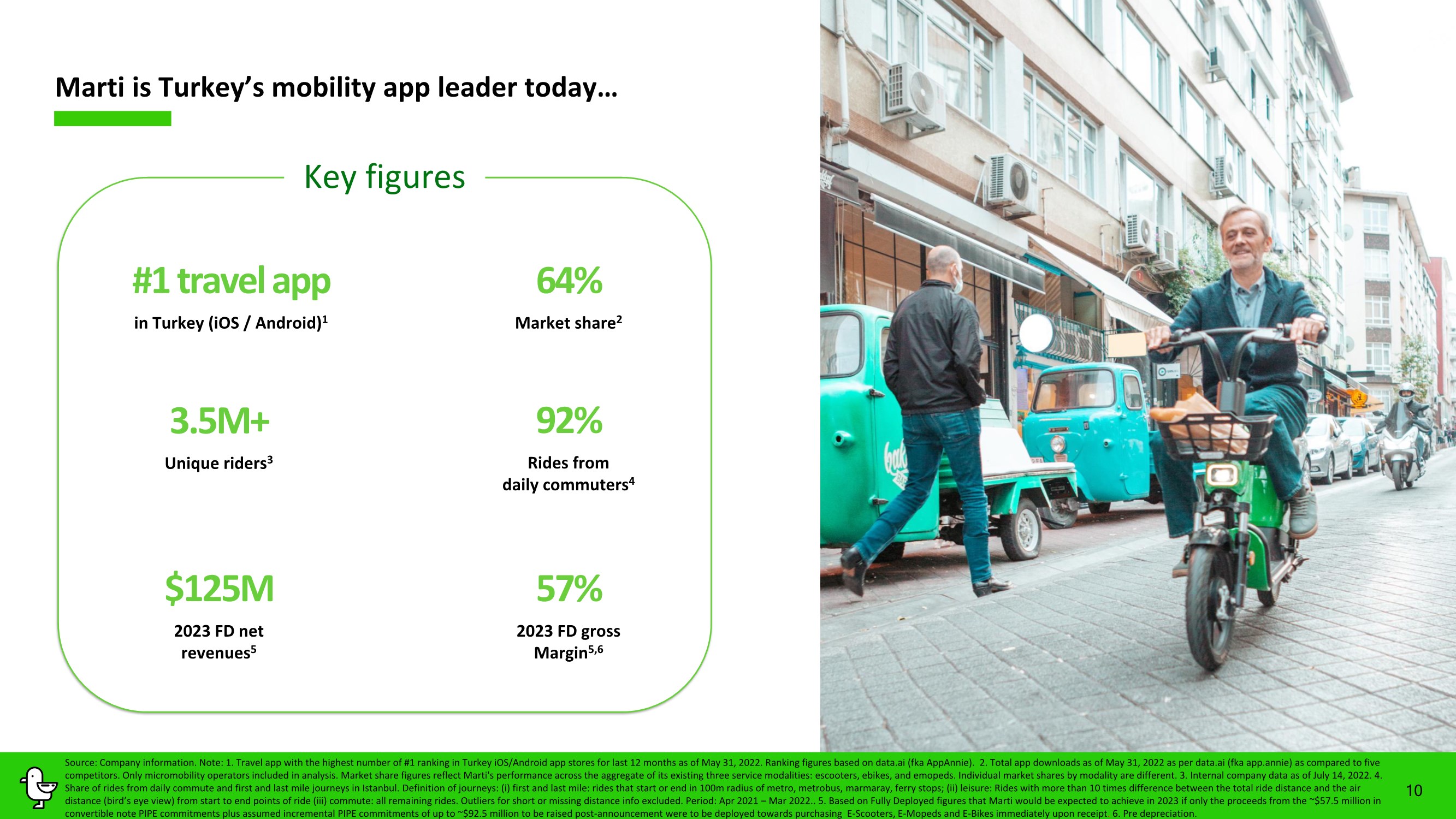

| 10 Marti is Turkey’s mobility app leader today… Key figures #1 travel app in Turkey (iOS / Android)1 3.5M+ Unique riders3 57% 2023 FD gross Margin5,6 92% Rides from daily commuters4 $125M 2023 FD net revenues5 64% Market share2 Source: Company information. Note: 1. Travel app with the highest number of #1 ranking in Turkey iOS/Android app stores for last 12 months as of May 31, 2022. Ranking figures based on data.ai (fka AppAnnie). 2. Total app downloads as of May 31, 2022 as per data.ai (fka app.annie) as compared to five competitors. Only micromobility operators included in analysis. Market share figures reflect Marti's performance across the aggregate of its existing three service modalities: escooters, ebikes, and emopeds. Individual market shares by modality are different. 3. Internal company data as of July 14, 2022. 4. Share of rides from daily commute and first and last mile journeys in Istanbul. Definition of journeys: (i) first and last mile: rides that start or end in 100m radius of metro, metrobus, marmaray, ferry stops; (ii) leisure: Rides with more than 10 times difference between the total ride distance and the air distance (bird’s eye view) from start to end points of ride (iii) commute: all remaining rides. Outliers for short or missing distance info excluded. Period: Apr 2021 – Mar 2022.. 5. Based on Fully Deployed figures that Marti would be expected to achieve in 2023 if only the proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement were to be deployed towards purchasing E-Scooters, E-Mopeds and E-Bikes immediately upon receipt. 6. Pre depreciation. |

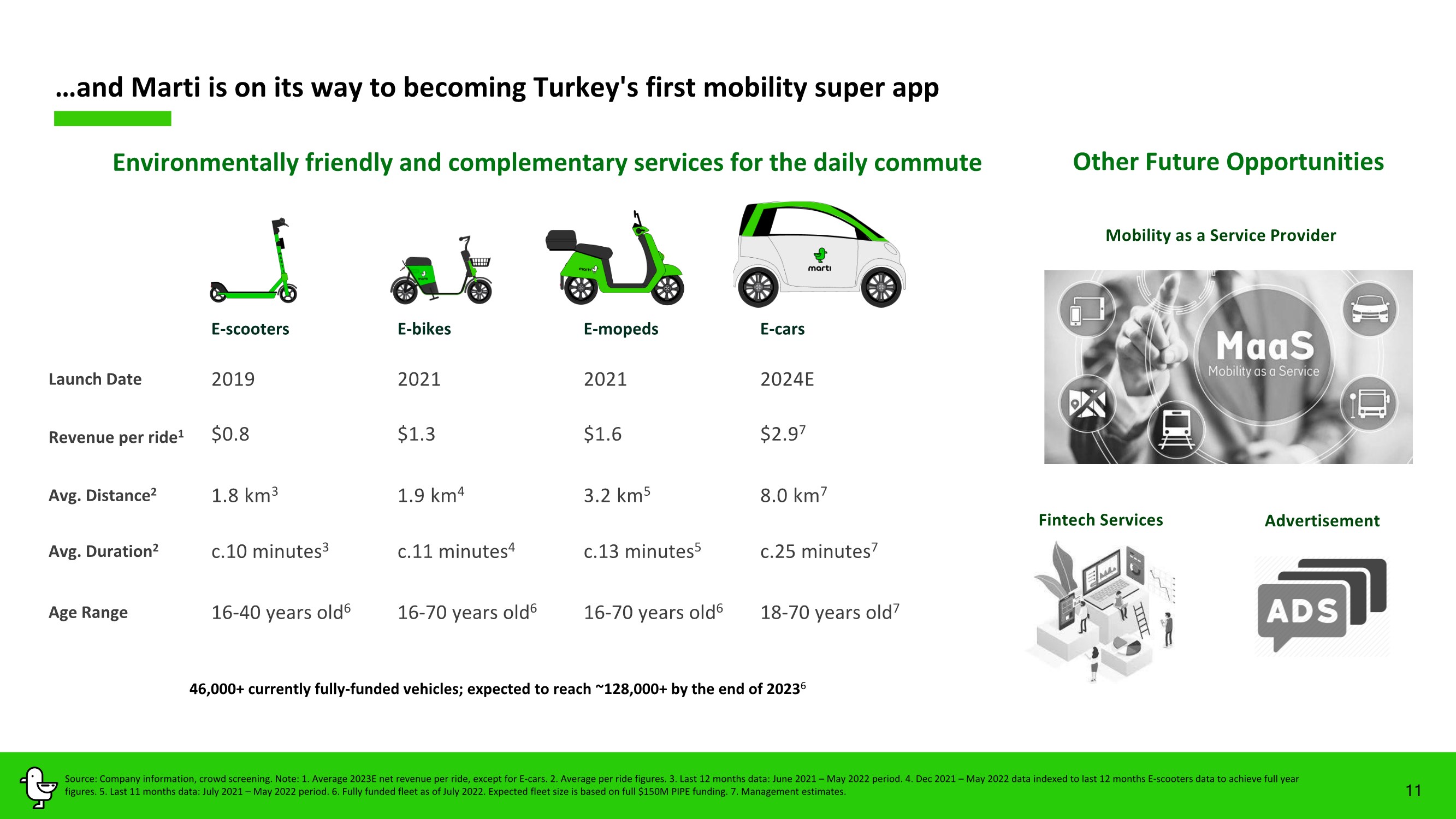

| Environmentally friendly and complementary services for the daily commute …and Marti is on its way to becoming Turkey's first mobility super app 46,000+ currently fully-funded vehicles; expected to reach ~128,000+ by the end of 20236 Other Future Opportunities Advertisement Fintech Services Mobility as a Service Provider E-scooters E-bikes E-mopeds E-cars Launch Date 2019 2021 2021 2024E Revenue per ride1 $0.8 $1.3 $1.6 $2.97 Avg. Distance2 1.8 km3 1.9 km4 3.2 km5 8.0 km7 Avg. Duration2 c.10 minutes3 c.11 minutes4 c.13 minutes5 c.25 minutes7 Age Range 16-40 years old6 16-70 years old6 16-70 years old6 18-70 years old7 11 Source: Company information, crowd screening. Note: 1. Average 2023E net revenue per ride, except for E-cars. 2. Average per ride figures. 3. Last 12 months data: June 2021 – May 2022 period. 4. Dec 2021 – May 2022 data indexed to last 12 months E-scooters data to achieve full year figures. 5. Last 11 months data: July 2021 – May 2022 period. 6. Fully funded fleet as of July 2022. Expected fleet size is based on full $150M PIPE funding. 7. Management estimates. |

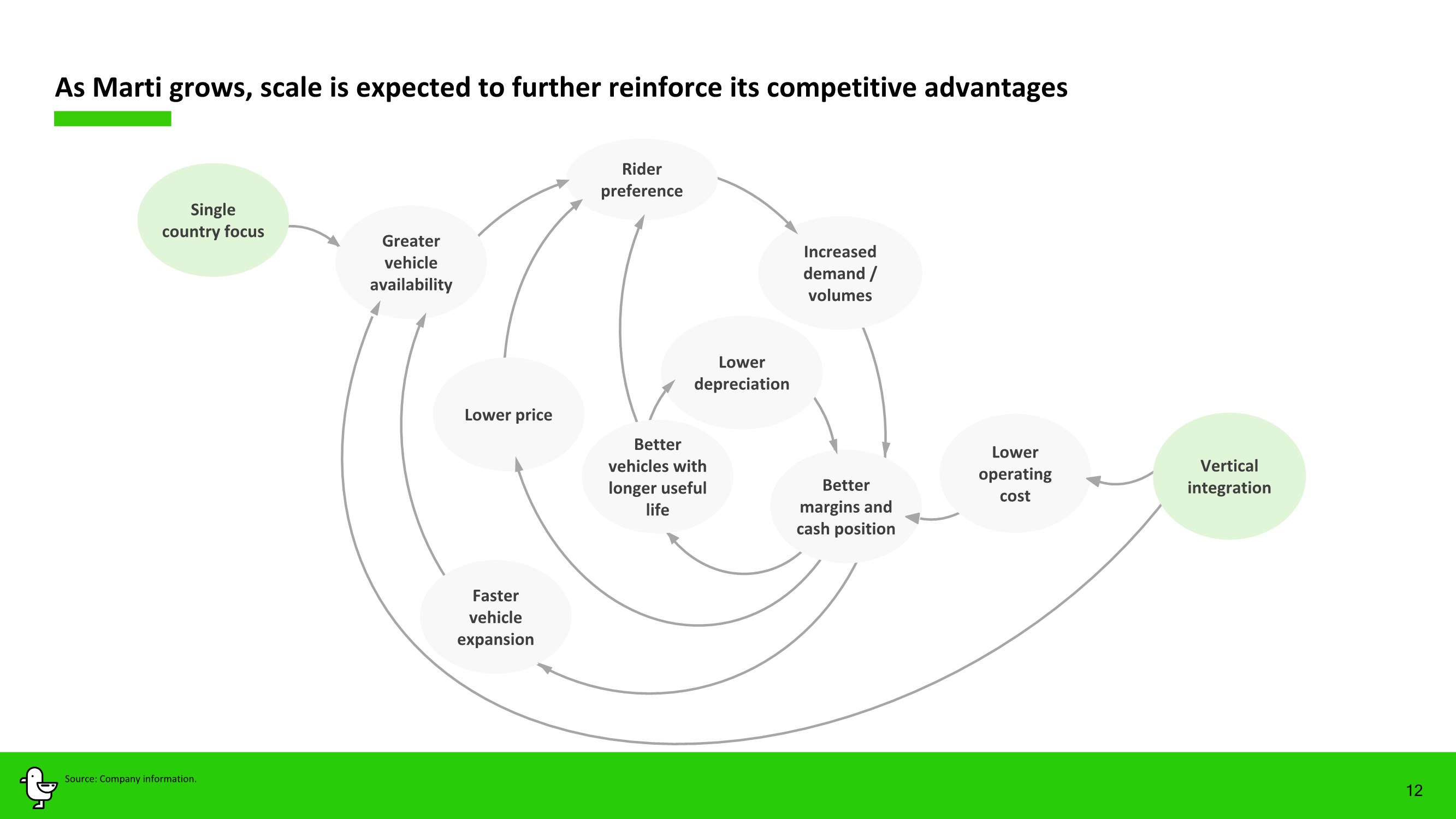

| Lower depreciation Single country focus Greater vehicle availability Lower operating cost Rider preference Increased demand / volumes Lower price Better margins and cash position Faster vehicle expansion Better vehicles with longer useful life Vertical integration 12 As Marti grows, scale is expected to further reinforce its competitive advantages Source: Company information. |

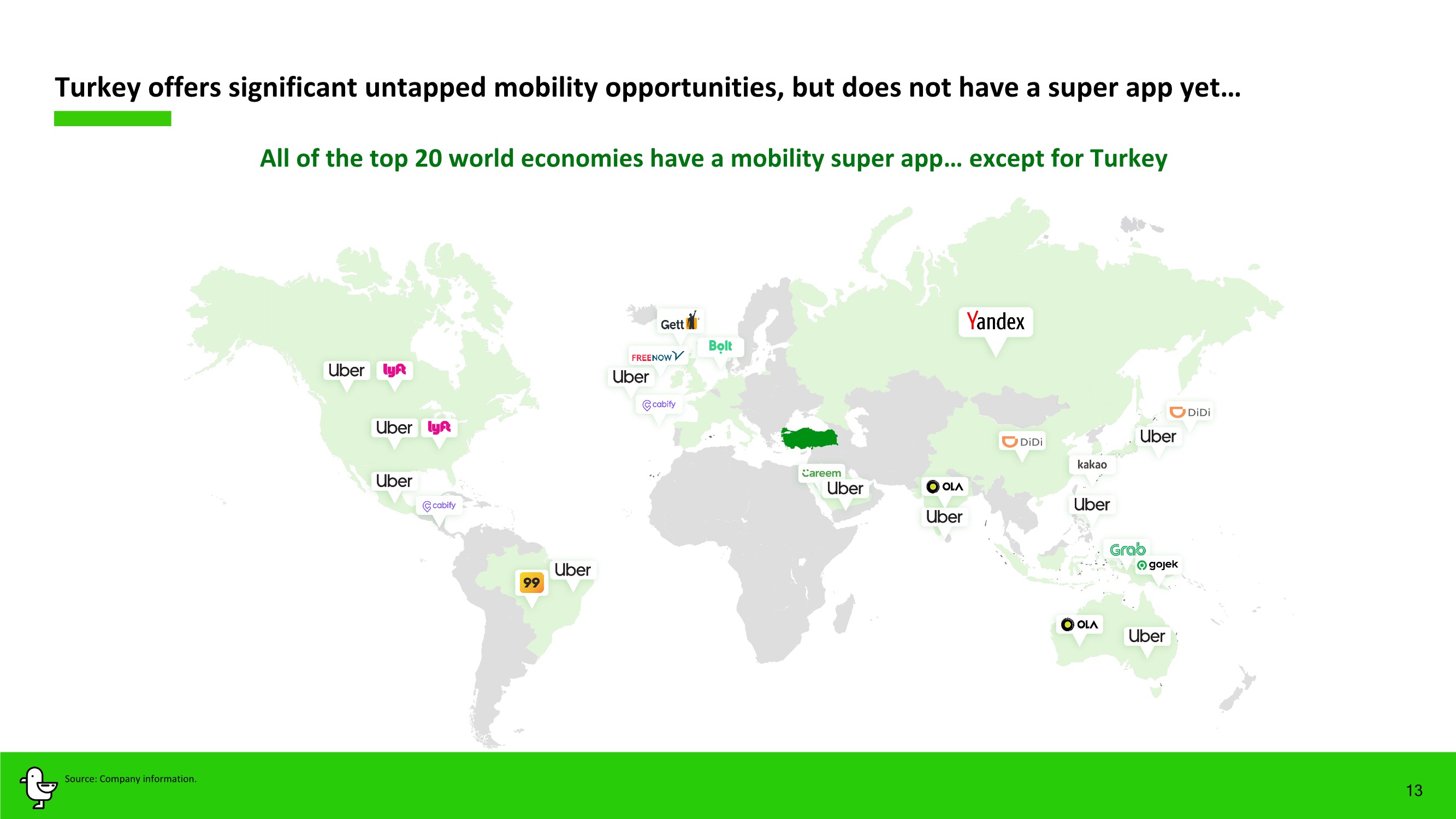

| All of the top 20 world economies have a mobility super app… except for Turkey Turkey offers significant untapped mobility opportunities, but does not have a super app yet… Source: Company information. 13 |

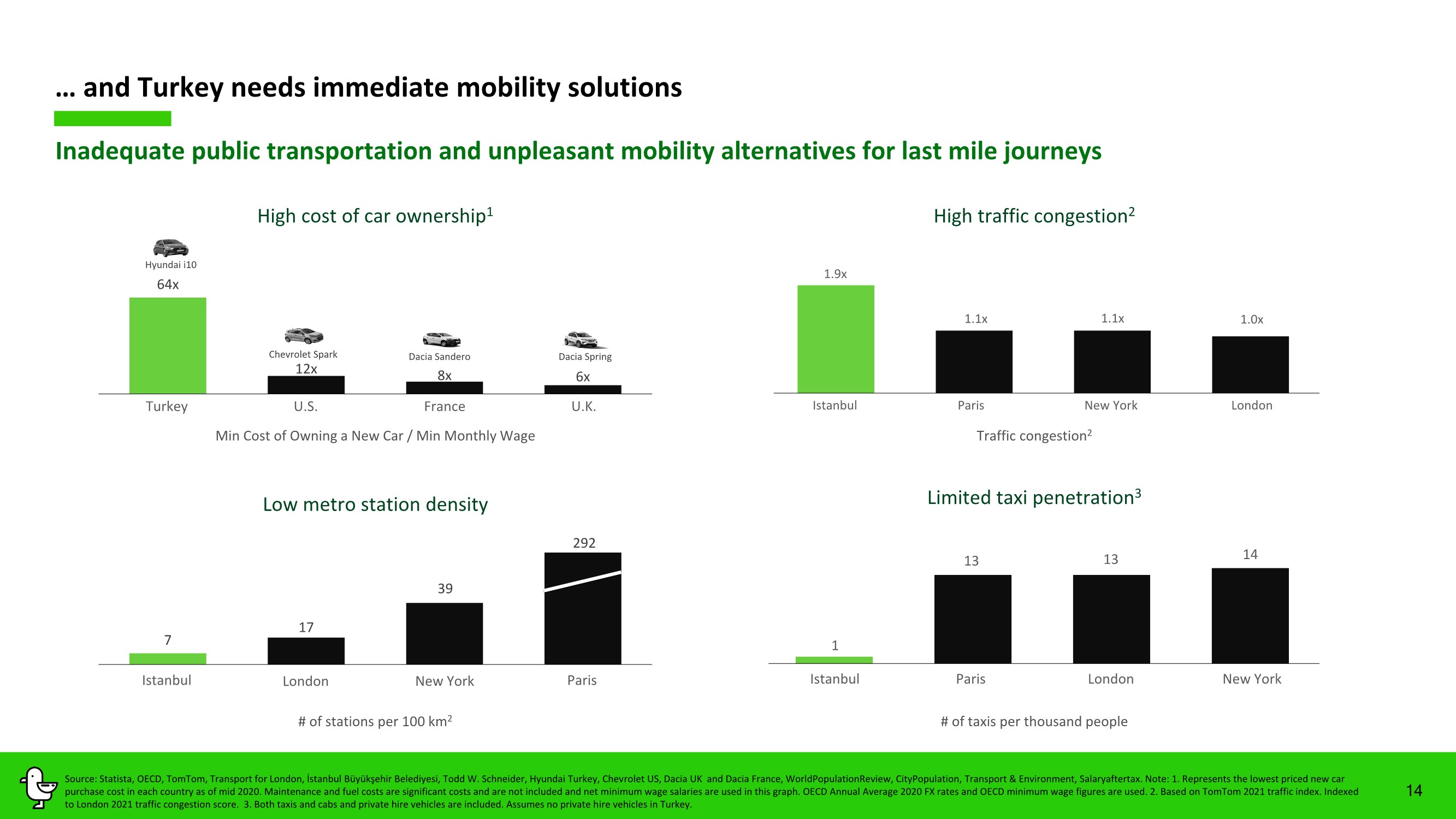

| 14 64x 12x 8x 6x Inadequate public transportation and unpleasant mobility alternatives for last mile journeys … and Turkey needs immediate mobility solutions High cost of car ownership1 Dacia Sandero Dacia Spring Chevrolet Spark Hyundai i10 Min Cost of Owning a New Car / Min Monthly Wage Low metro station density Istanbul Paris London New York Turkey U.K. U.S. France 7 17 39 292 Limited taxi penetration3 # of stations per 100 km2 1 13 13 14 0 2 4 6 8 10 12 14 16 London New York Paris Istanbul # of taxis per thousand people Source: Statista, OECD, TomTom, Transport for London, İstanbul Büyükşehir Belediyesi, Todd W. Schneider, Hyundai Turkey, Chevrolet US, Dacia UK and Dacia France, WorldPopulationReview, CityPopulation, Transport & Environment, Salaryaftertax. Note: 1. Represents the lowest priced new car purchase cost in each country as of mid 2020. Maintenance and fuel costs are significant costs and are not included and net minimum wage salaries are used in this graph. OECD Annual Average 2020 FX rates and OECD minimum wage figures are used. 2. Based on TomTom 2021 traffic index. Indexed to London 2021 traffic congestion score. 3. Both taxis and cabs and private hire vehicles are included. Assumes no private hire vehicles in Turkey. High traffic congestion2 1.9x 1.1x 1.1x 1.0x 0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0 New York London Paris Istanbul Traffic congestion2 |

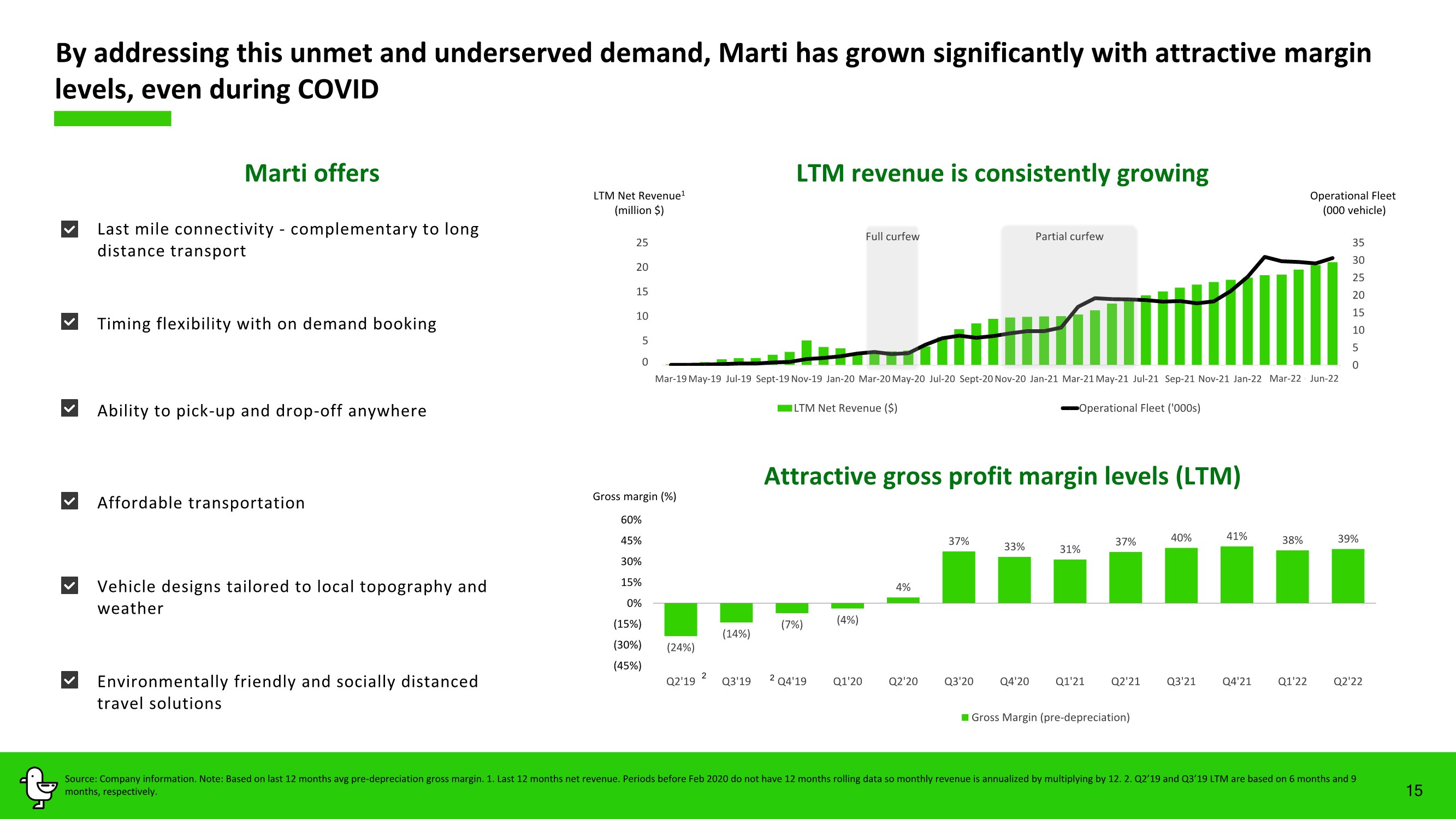

| 0 5 10 15 20 25 30 35 '- 5 10 15 20 25 Mar-19May-19 Jul-19 Sept-19Nov-19 Jan-20 Mar-20May-20 Jul-20 Sept-20Nov-20 Jan-21 Mar-21May-21 Jul-21 Sep-21 Nov-21 Jan-22 Mar-22May-22 LTM Net Revenue ($) Operational Fleet ('000s) 15 (24%) (14%) (7%) (4%) 4% 37% 33% 31% 37% 40% 41% 38% 39% (45%) (30%) (15%) 0% 15% 30% 45% 60% Q2'19 Q3'19 Q4'19 Q1'20 Q2'20 Q3'20 Q4'20 Q1'21 Q2'21 Q3'21 Q4'21 Q1'22 Q2'22 Gross Margin (pre-depreciation) 2 Attractive gross profit margin levels (LTM) By addressing this unmet and underserved demand, Marti has grown significantly with attractive margin levels, even during COVID 2 LTM revenue is consistently growing Last mile connectivity - complementary to long distance transport Timing flexibility with on demand booking Ability to pick-up and drop-off anywhere Affordable transportation Vehicle designs tailored to local topography and weather Environmentally friendly and socially distanced travel solutions Marti offers Source: Company information. Note: Based on last 12 months avg pre-depreciation gross margin. 1. Last 12 months net revenue. Periods before Feb 2020 do not have 12 months rolling data so monthly revenue is annualized by multiplying by 12. 2. Q2’19 and Q3’19 LTM are based on 6 months and 9 months, respectively. 0 LTM Net Revenue1 (million $) Operational Fleet (000 vehicle) Gross margin (%) Full curfew Partial curfew Mar-22 Jun-22 |

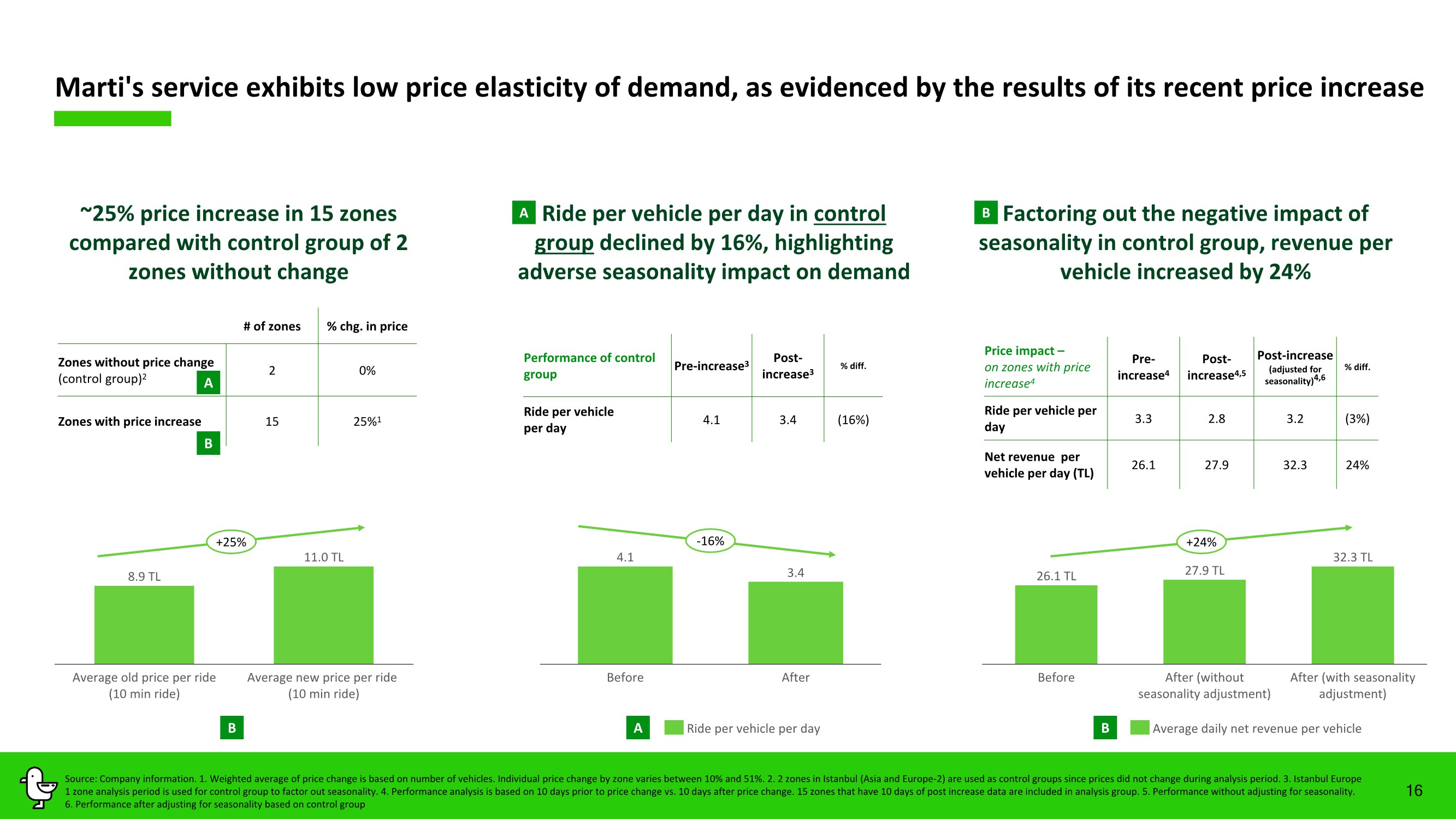

| 16 Source: Company information. 1. Weighted average of price change is based on number of vehicles. Individual price change by zone varies between 10% and 51%. 2. 2 zones in Istanbul (Asia and Europe-2) are used as control groups since prices did not change during analysis period. 3. Istanbul Europe 1 zone analysis period is used for control group to factor out seasonality. 4. Performance analysis is based on 10 days prior to price change vs. 10 days after price change. 15 zones that have 10 days of post increase data are included in analysis group. 5. Performance without adjusting for seasonality. 6. Performance after adjusting for seasonality based on control group # of zones % chg. in price Zones without price change (control group)2 2 0% Zones with price increase 15 25%1 ~25% price increase in 15 zones compared with control group of 2 zones without change Factoring out the negative impact of seasonality in control group, revenue per vehicle increased by 24% 26.1 TL 27.9 TL 32.3 TL Before After (without seasonality adjustment) After (with seasonality adjustment) Average daily net revenue per vehicle 8.9 TL 11.0 TL Average old price per ride (10 min ride) Average new price per ride (10 min ride) Price impact – on zones with price increase4 Pre- increase4 Post- increase4,5 Post-increase (adjusted for seasonality)4,6 % diff. Ride per vehicle per day 3.3 2.8 3.2 (3%) Net revenue per vehicle per day (TL) 26.1 27.9 32.3 24% Ride per vehicle per day in control group declined by 16%, highlighting adverse seasonality impact on demand Performance of control group Pre-increase3 Post- increase3 % diff. Ride per vehicle per day 4.1 3.4 (16%) 4.1 3.4 Before After Ride per vehicle per day B A BA ABB +25% +24%-16% Marti's service exhibits low price elasticity of demand, as evidenced by the results of its recent price increase |

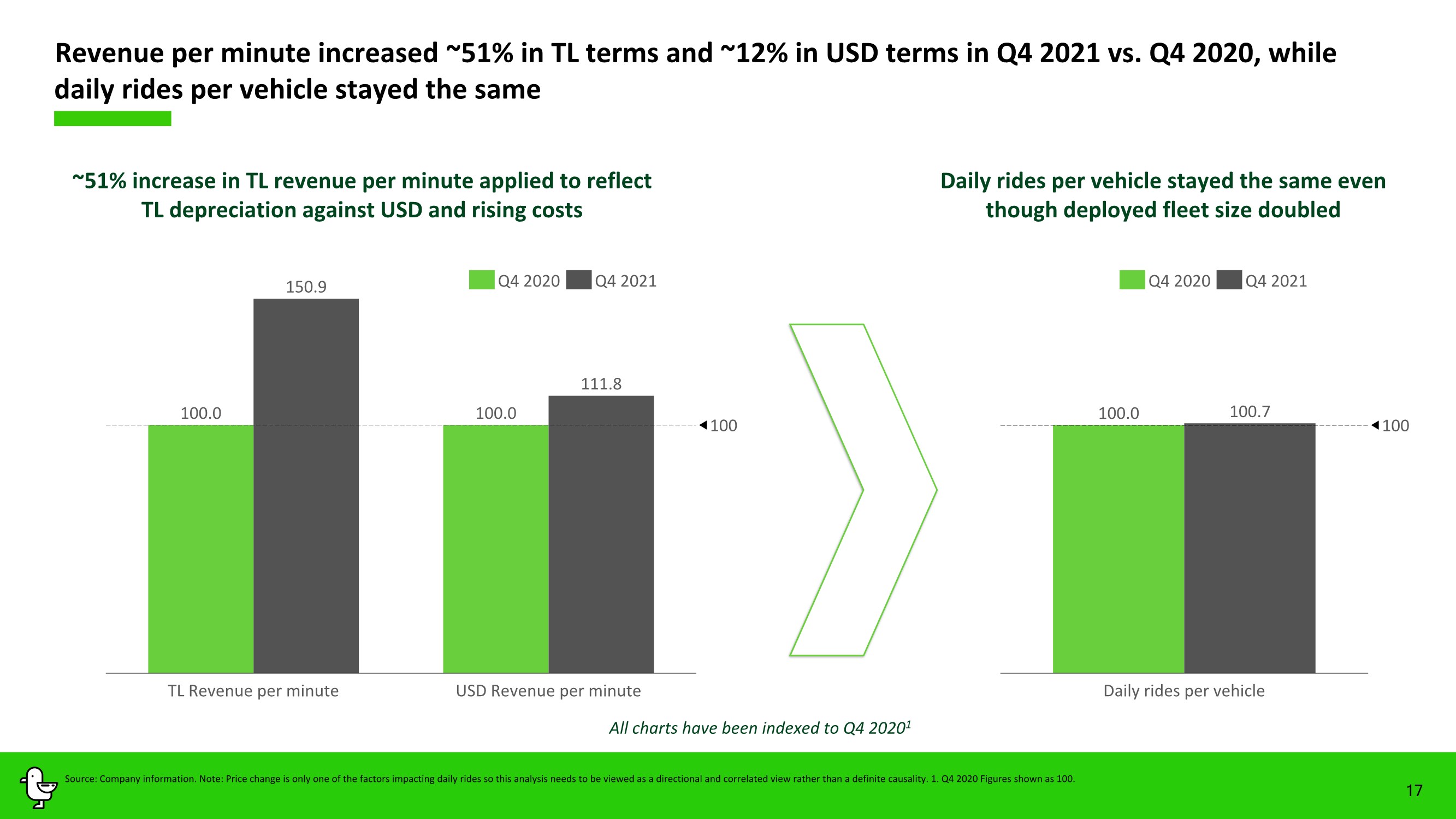

| Revenue per minute increased ~51% in TL terms and ~12% in USD terms in Q4 2021 vs. Q4 2020, while daily rides per vehicle stayed the same 17 Source: Company information. Note: Price change is only one of the factors impacting daily rides so this analysis needs to be viewed as a directional and correlated view rather than a definite causality. 1. Q4 2020 Figures shown as 100. 100.0 100.0 150.9 111.8 100 TL Revenue per minute USD Revenue per minute Q4 2020 Q4 2021 100.0 100.7 100 Daily rides per vehicle Q4 2020 Q4 2021 ~51% increase in TL revenue per minute applied to reflect TL depreciation against USD and rising costs Daily rides per vehicle stayed the same even though deployed fleet size doubled All charts have been indexed to Q4 20201 |

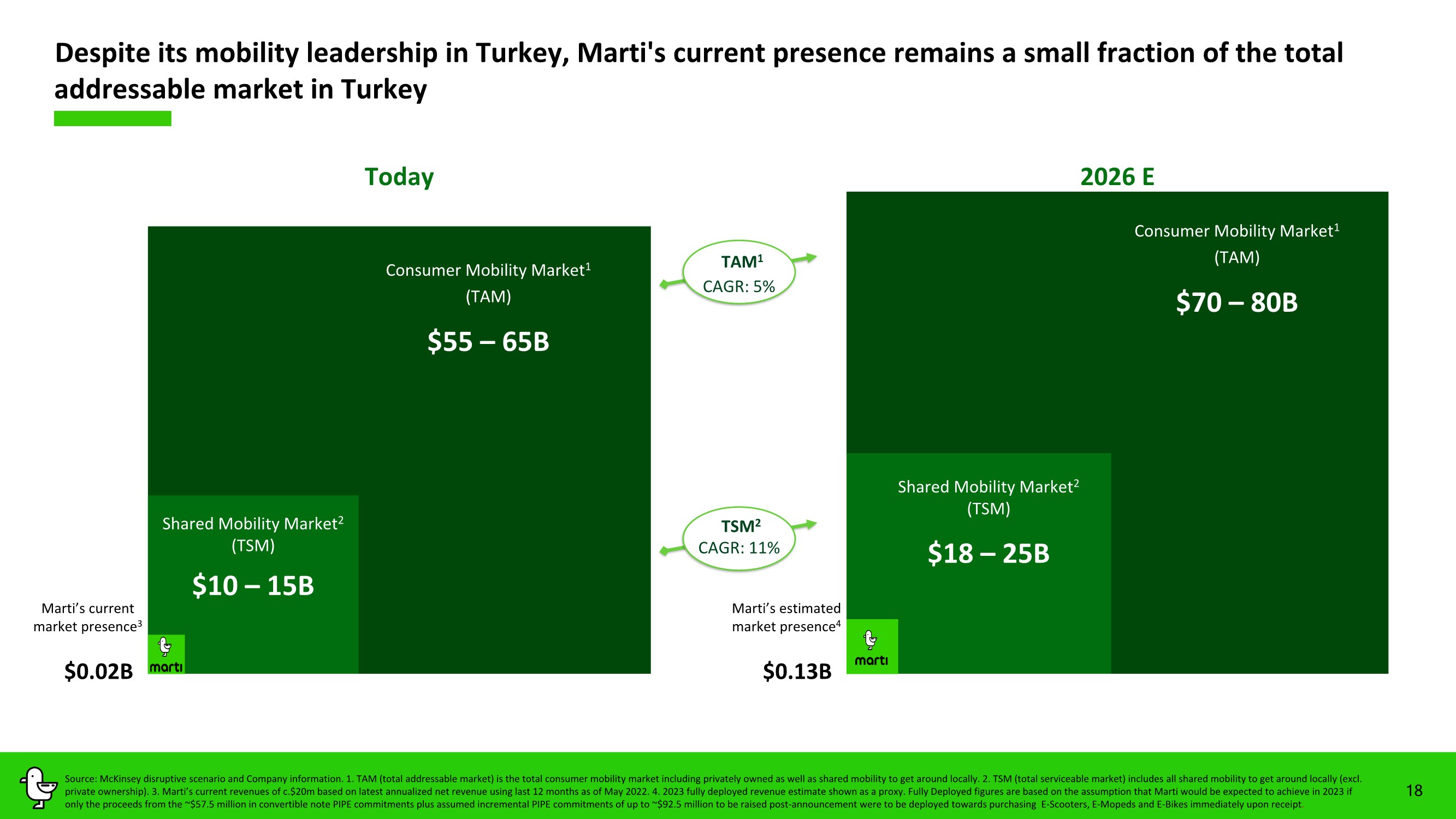

| Despite its mobility leadership in Turkey, Marti's current presence remains a small fraction of the total addressable market in Turkey 18 Marti’s current market presence3 $0.02B $55 – 65B Consumer Mobility Market1 (TAM) Shared Mobility Market2 (TSM) $10 – 15B Marti’s estimated market presence4 $0.13B $70 – 80B Consumer Mobility Market1 (TAM) Shared Mobility Market2 (TSM) $18 – 25B Today 2026 E Source: McKinsey disruptive scenario and Company information. 1. TAM (total addressable market) is the total consumer mobility market including privately owned as well as shared mobility to get around locally. 2. TSM (total serviceable market) includes all shared mobility to get around locally (excl. private ownership). 3. Marti’s current revenues of c.$20m based on latest annualized net revenue using last 12 months as of May 2022. 4. 2023 fully deployed revenue estimate shown as a proxy. Fully Deployed figures are based on the assumption that Marti would be expected to achieve in 2023 if only the proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement were to be deployed towards purchasing E-Scooters, E-Mopeds and E-Bikes immediately upon receipt. CAGR: 5% TAM1 CAGR: 11% TSM2 |

| 1. Highly attractive market demographics 2. Clear market leader 3. Strong customer retention, reinforced by scale 4. Vertically integrated business model driving lower costs and higher revenues 5. Best-in-class unit economics 6. Constructive regulatory framework 7. Strong ESG fundamentals 19 Key investment highlights Source: Company information. Note: Key investment highlight #5 is in comparison to Bird and Helbiz. |

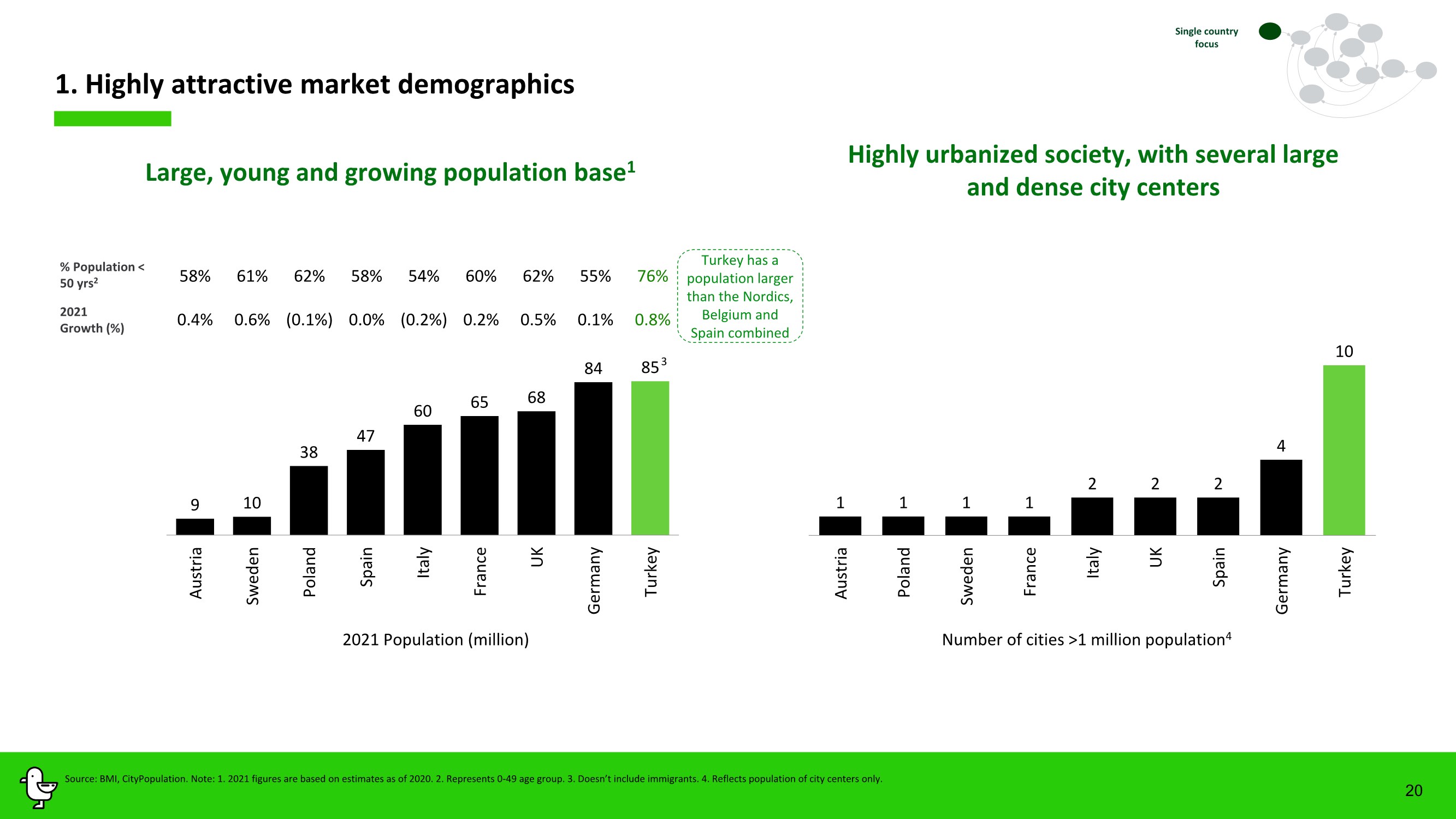

| 1 1 1 1 2 2 2 4 10 Austria Poland Sweden France Italy UK Spain Germany Turkey 20 1. Highly attractive market demographics 9 10 38 47 60 65 68 84 85 Austria Sweden Poland Spain Italy France UK Germany Turkey % Population < 50 yrs2 2021 Growth (%) 3 Source: BMI, CityPopulation. Note: 1. 2021 figures are based on estimates as of 2020. 2. Represents 0-49 age group. 3. Doesn’t include immigrants. 4. Reflects population of city centers only. Highly urbanized society, with several large and dense city centers Single country focus Large, young and growing population base1 2021 Population (million) Number of cities >1 million population4 58% 61% 62% 58% 54% 60% 62% 55% 76% 0.4% 0.6% (0.1%) 0.0% (0.2%) 0.2% 0.5% 0.1% 0.8% Turkey has a population larger than the Nordics, Belgium and Spain combined |

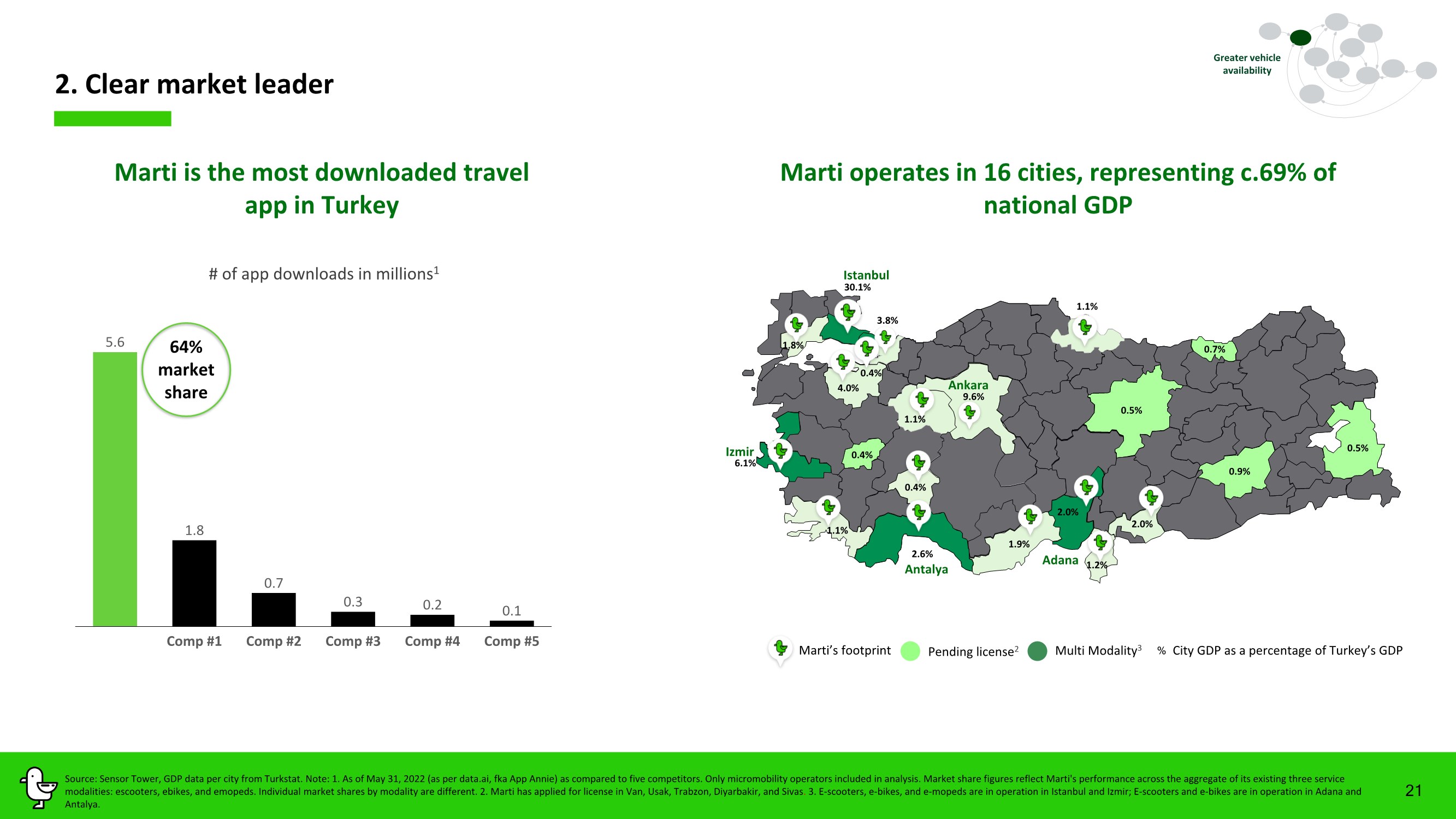

| 21 Source: Sensor Tower, GDP data per city from Turkstat. Note: 1. As of May 31, 2022 (as per data.ai, fka App Annie) as compared to five competitors. Only micromobility operators included in analysis. Market share figures reflect Marti's performance across the aggregate of its existing three service modalities: escooters, ebikes, and emopeds. Individual market shares by modality are different. 2. Marti has applied for license in Van, Usak, Trabzon, Diyarbakir, and Sivas. 3. E-scooters, e-bikes, and e-mopeds are in operation in Istanbul and Izmir; E-scooters and e-bikes are in operation in Adana and Antalya. Marti is the most downloaded travel app in Turkey 64% market share 2. Clear market leader Greater vehicle availability Marti operates in 16 cities, representing c.69% of national GDP City GDP as a percentage of Turkey’s GDP % Multi Modality3 Pending license2 Marti’s footprint 30.1% 3.8% 9.6% 1.1% 2.6% 1.9% 6.1% 2.0% 2.0% 1.2% 1.1% 1.1% 4.0% 0.4% 1.8% Istanbul Izmir Ankara Antalya 0.4% Adana 0.5% 0.7% 0.5% 0.9% 0.4% 5.6 1.8 0.7 0.3 0.2 0.1 Comp #3 Comp #1 Comp #2 Comp #4 Comp #5 # of app downloads in millions1 |

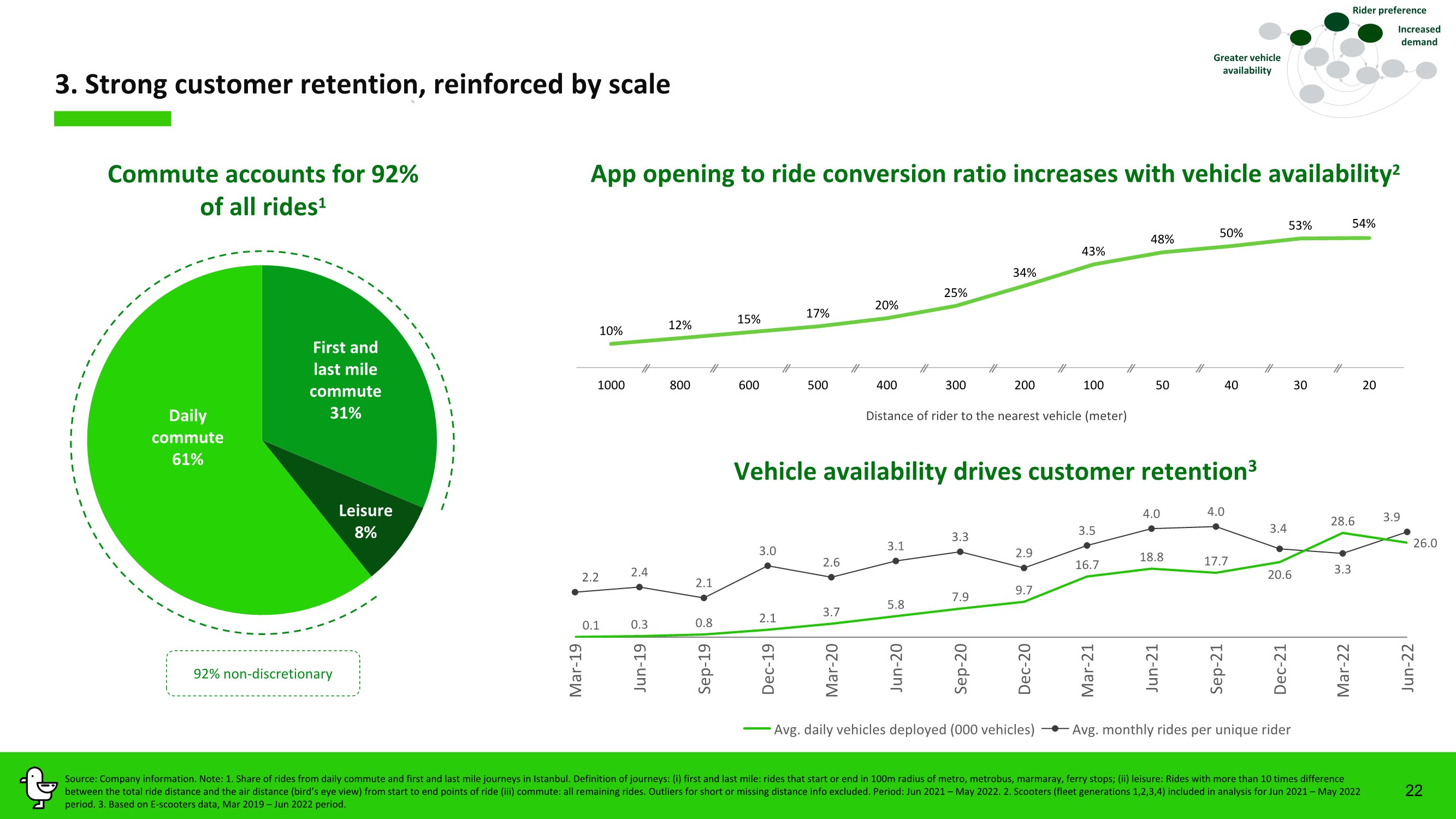

| 3. Strong customer retention, reinforced by scale 22 Vehicle availability drives customer retention3 App opening to ride conversion ratio increases with vehicle availability2 10% 12% 15% 17% 20% 25% 34% 43% 48% 50% 53% 54% 1000 800 600 500 400 300 200 100 50 40 30 20 Distance of rider to the nearest vehicle (meter) Rider preference Increased demand Commute accounts for 92% of all rides1 Source: Company information. Note: 1. Share of rides from daily commute and first and last mile journeys in Istanbul. Definition of journeys: (i) first and last mile: rides that start or end in 100m radius of metro, metrobus, marmaray, ferry stops; (ii) leisure: Rides with more than 10 times difference between the total ride distance and the air distance (bird’s eye view) from start to end points of ride (iii) commute: all remaining rides. Outliers for short or missing distance info excluded. Period: Jun 2021 – May 2022. 2. Scooters (fleet generations 1,2,3,4) included in analysis for Jun 2021 – May 2022 period. 3. Based on E-scooters data, Mar 2019 – Jun 2022 period. 92% non-discretionary Greater vehicle availability Daily commute 61% First and last mile commute 31% Leisure 8% 2.2 2.4 3.0 2.6 3.1 3.3 3.5 4.0 4.0 3.4 3.3 3.9 Jun - 20 Sep - 19 Jun - 19 Jun - 21 Dec - 19 Mar - 21 Mar - 20 Dec - 20 Sep - 20 Sep - 21 Dec - 21 Jun - 22 Mar - 22 Mar - 19 3.7 28.6 0.1 0.3 0.8 2.1 2.1 5.8 7.9 9.7 2.9 16.7 18.8 17.7 20.6 26.0 Avg. daily vehicles deployed (000 vehicles) Avg. monthly rides per unique rider |

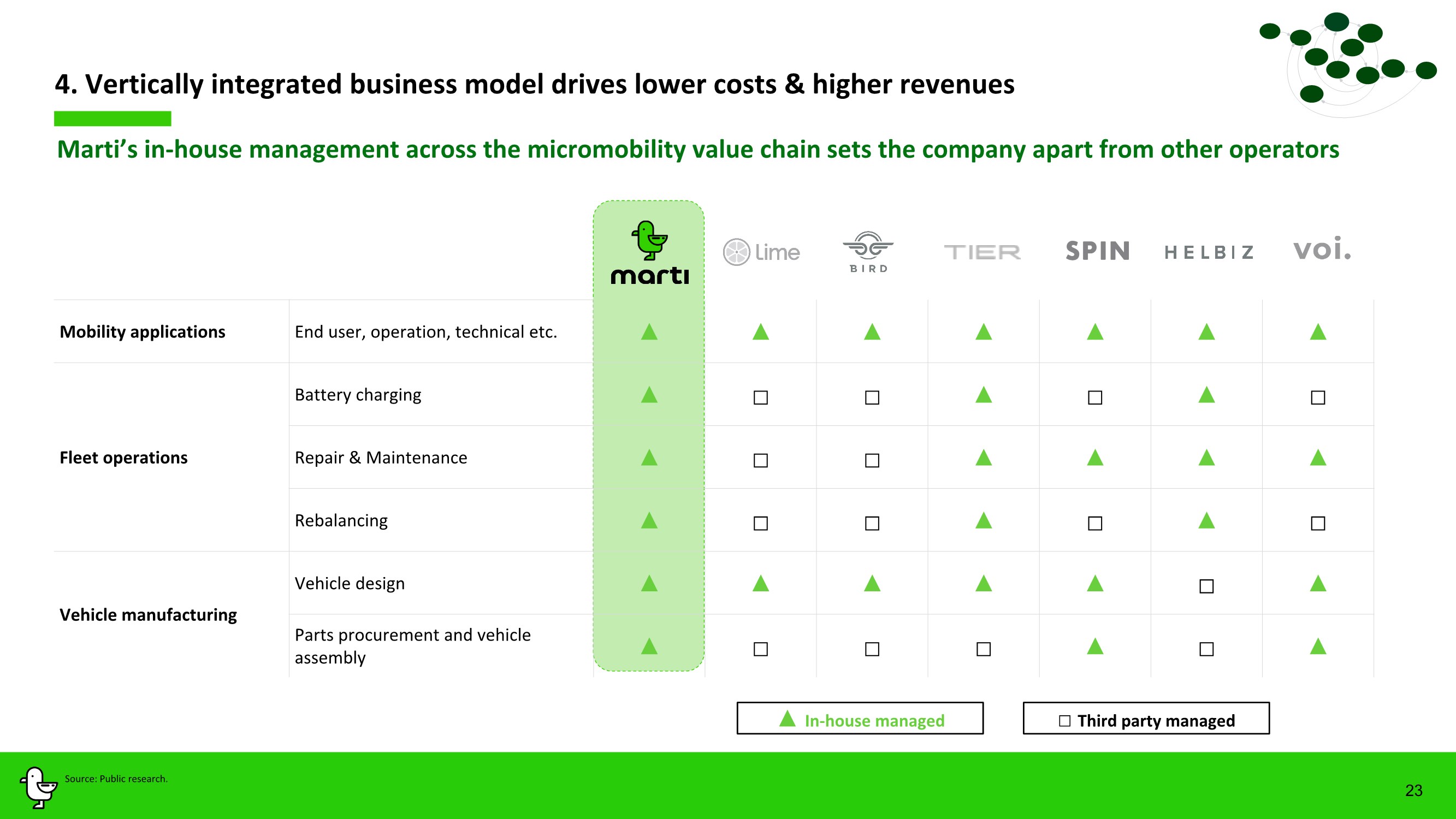

| 23 4. Vertically integrated business model drives lower costs & higher revenues Mobility applications End user, operation, technical etc. ▲ ▲ ▲ ▲ ▲ ▲ ▲ Fleet operations Battery charging ▲ □ □ ▲ □ ▲ □ Repair & Maintenance ▲ □ □ ▲ ▲ ▲ ▲ Rebalancing ▲ □ □ ▲ □ ▲ □ Vehicle manufacturing Vehicle design ▲ ▲ ▲ ▲ ▲ □ ▲ Parts procurement and vehicle assembly ▲ □ □ □ ▲ □ ▲ Marti’s in-house management across the micromobility value chain sets the company apart from other operators Source: Public research. ▲ In-house managed □ Third party managed |

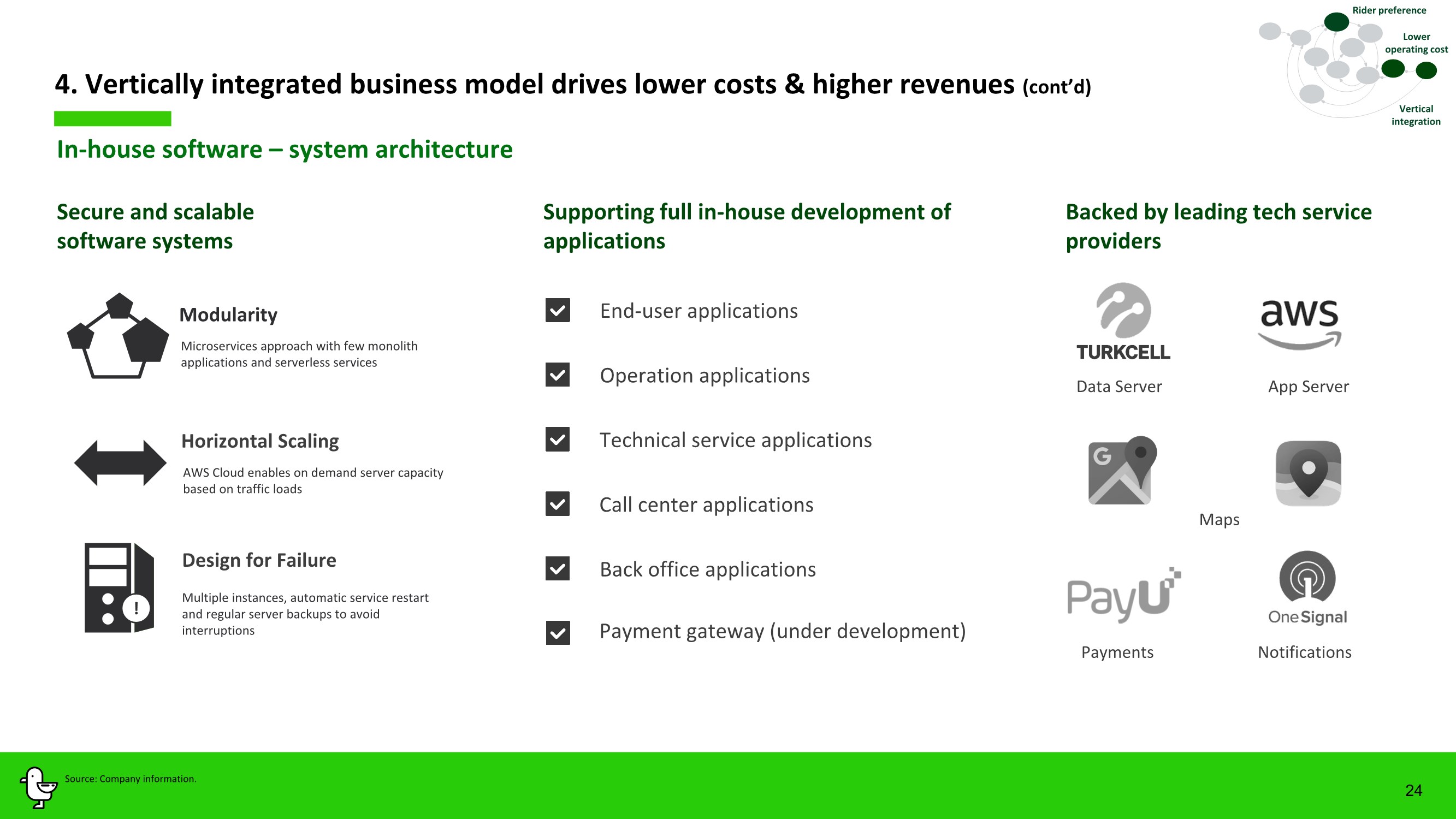

| 24 Maps Payments Notifications App Server Data Server Design for Failure ! Horizontal Scaling Secure and scalable software systems Multiple instances, automatic service restart and regular server backups to avoid interruptions Supporting full in-house development of applications Backed by leading tech service providers Modularity Microservices approach with few monolith applications and serverless services AWS Cloud enables on demand server capacity based on traffic loads 4. Vertically integrated business model drives lower costs & higher revenues (cont’d) In-house software – system architecture Vertical integration Source: Company information. Rider preference Back office applications Technical service applications Operation applications Call center applications End-user applications Payment gateway (under development) Lower operating cost |

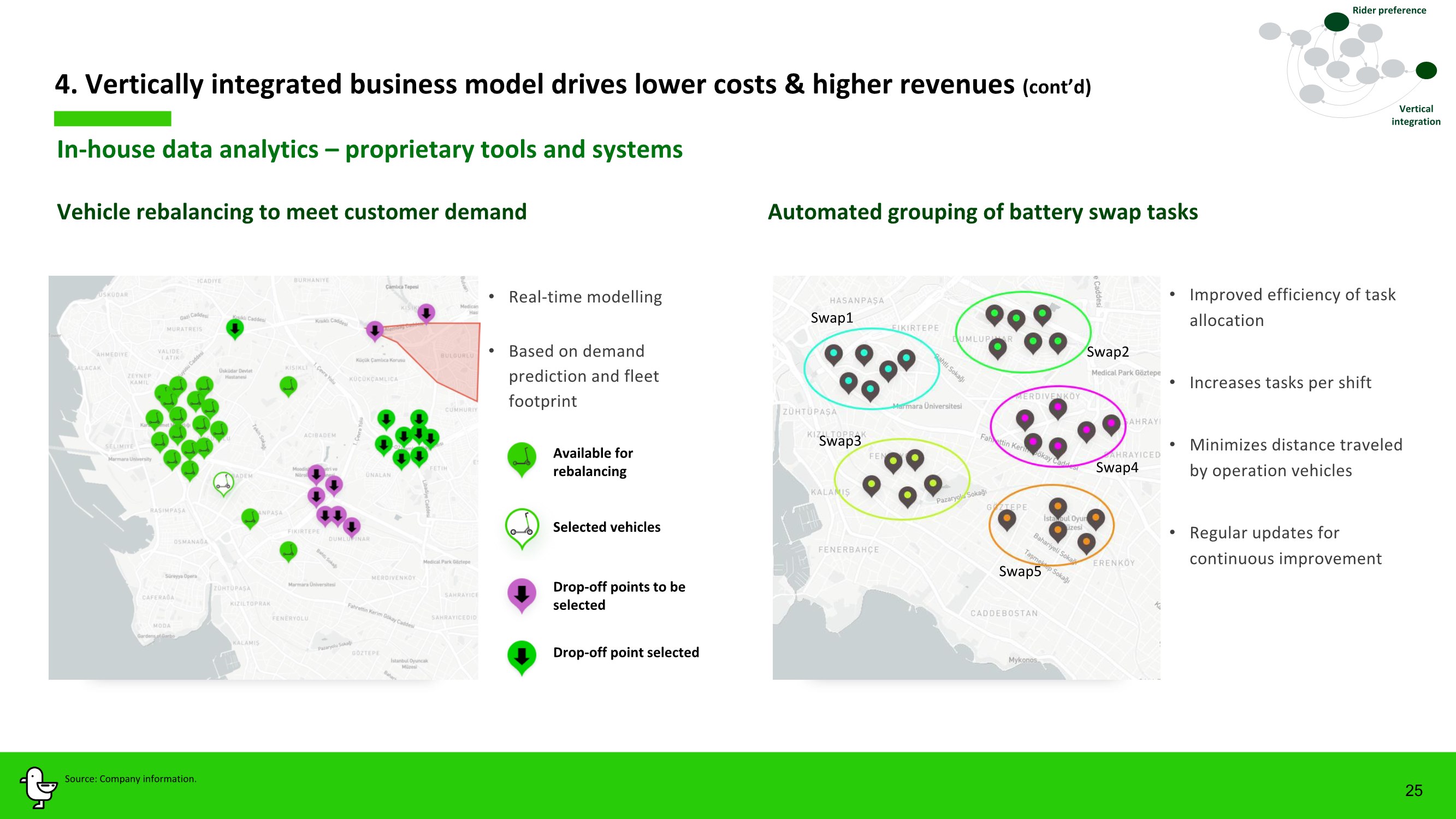

| 25 In-house data analytics – proprietary tools and systems 4. Vertically integrated business model drives lower costs & higher revenues (cont’d) Vehicle rebalancing to meet customer demand Automated grouping of battery swap tasks Swap1 Swap3 Swap5 Swap4 Swap2 Vertical integration • Real-time modelling • Based on demand prediction and fleet footprint • Improved efficiency of task allocation • Increases tasks per shift • Minimizes distance traveled by operation vehicles • Regular updates for continuous improvement Available for rebalancing Selected vehicles Drop-off points to be selected Drop-off point selected Source: Company information. Rider preference |

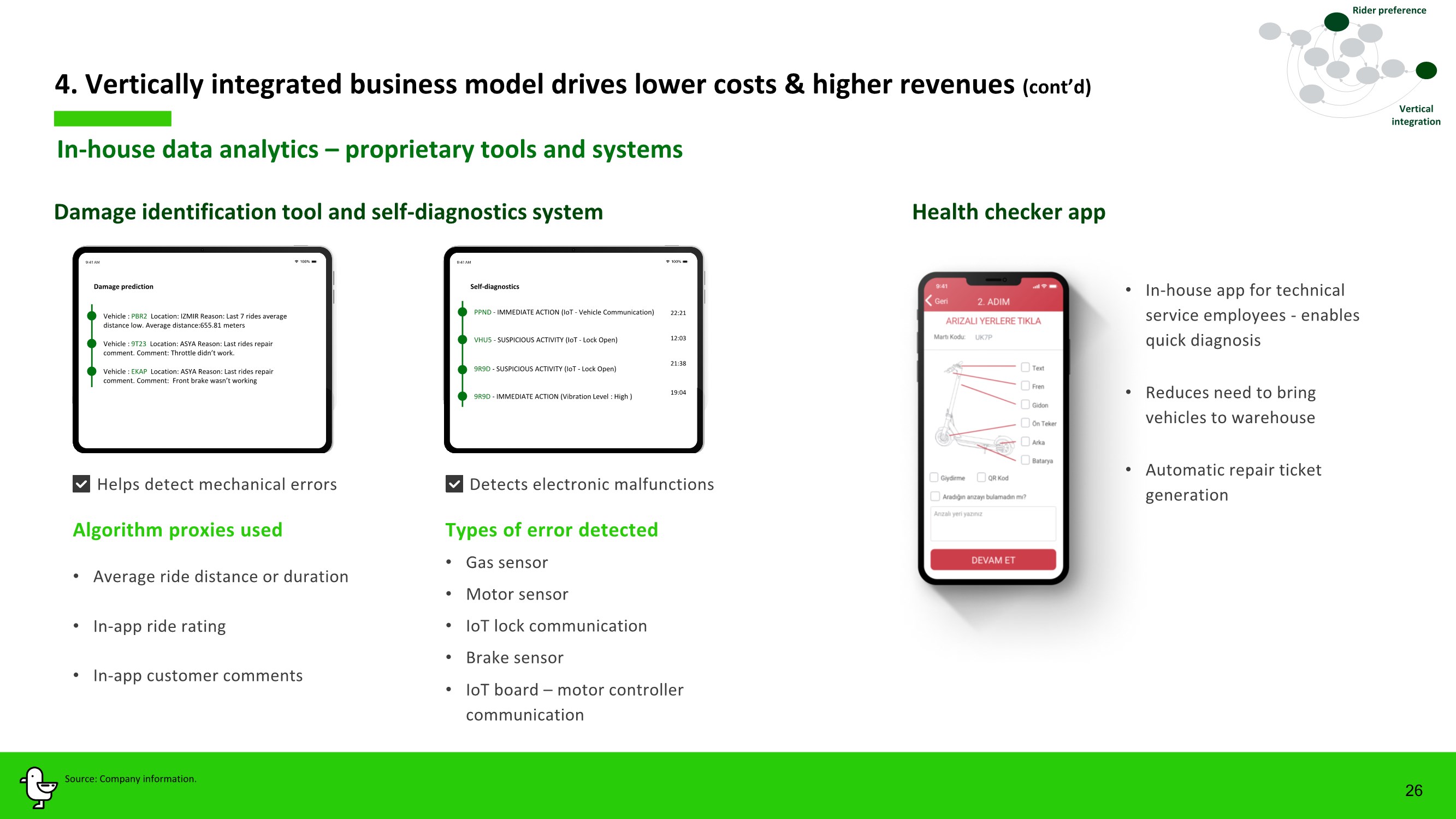

| 26 4. Vertically integrated business model drives lower costs & higher revenues (cont’d) Vertical integration Damage identification tool and self-diagnostics system Health checker app Vehicle : PBR2 Location: IZMIR Reason: Last 7 rides average distance low. Average distance:655.81 meters Vehicle : 9T23 Location: ASYA Reason: Last rides repair comment. Comment: Throttle didn’t work. Vehicle : EKAP Location: ASYA Reason: Last rides repair comment. Comment: Front brake wasn’t working Damage prediction PPND - IMMEDIATE ACTION (IoT - Vehicle Communication) VHU5 - SUSPICIOUS ACTIVITY (IoT - Lock Open) 9R9D - SUSPICIOUS ACTIVITY (IoT - Lock Open) 9R9D - IMMEDIATE ACTION (Vibration Level : High ) 22:21 12:03 21:38 19:04 Self-diagnostics • In-house app for technical service employees - enables quick diagnosis • Reduces need to bring vehicles to warehouse • Automatic repair ticket generation Types of error detected • Gas sensor • Motor sensor • Brake sensor • IoT lock communication • IoT board – motor controller communication Algorithm proxies used • Average ride distance or duration • In-app ride rating • In-app customer comments Helps detect mechanical errors Detects electronic malfunctions In-house data analytics – proprietary tools and systems Source: Company information. Rider preference |

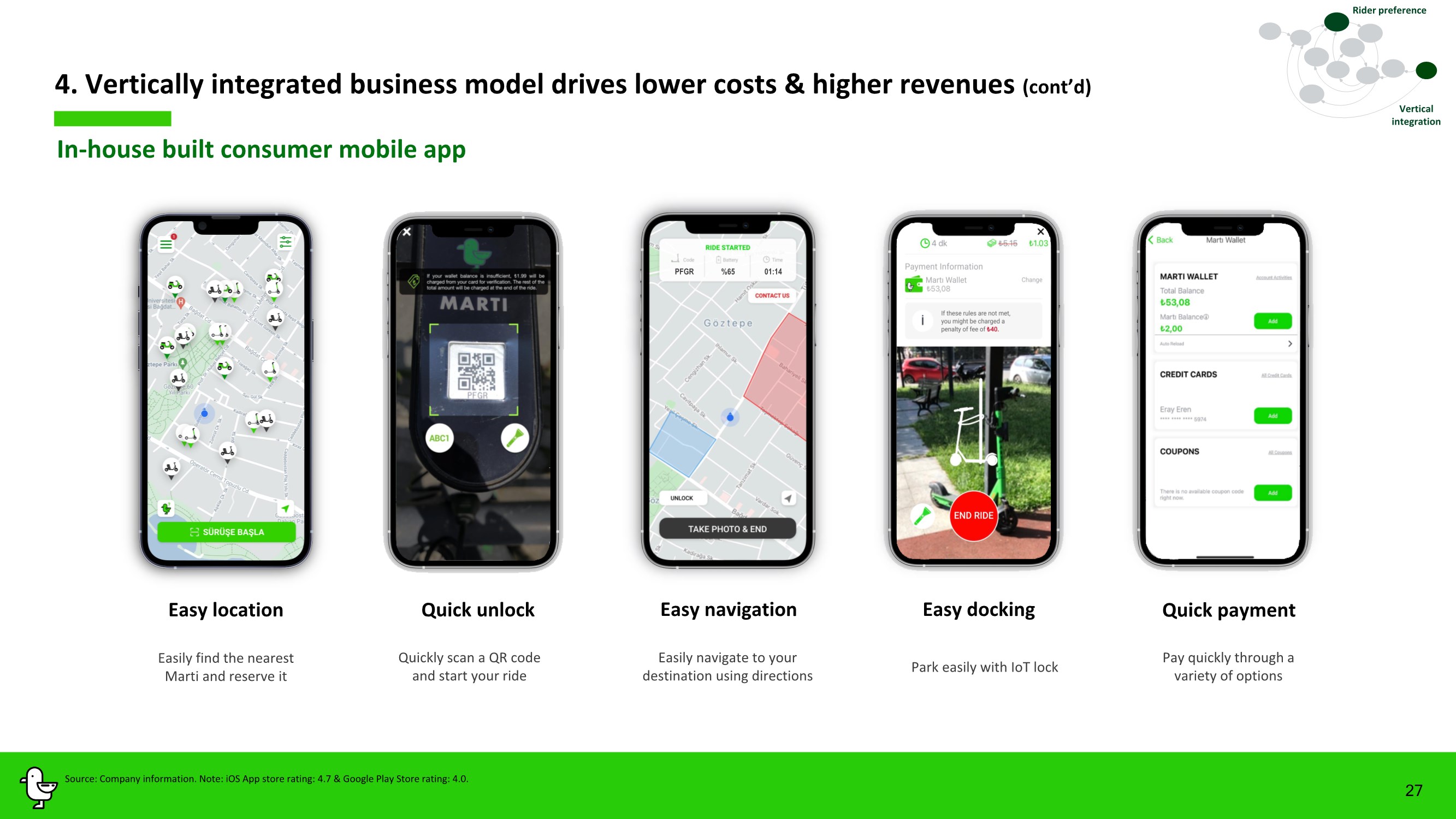

| In-house built consumer mobile app 4. Vertically integrated business model drives lower costs & higher revenues (cont’d) Vertical integration Easily find the nearest Marti and reserve it Quickly scan a QR code and start your ride Easily navigate to your destination using directions Park easily with IoT lock Pay quickly through a variety of options Quick unlock Easy navigation Easy docking Quick payment 27 Rider preference Source: Company information. Note: iOS App store rating: 4.7 & Google Play Store rating: 4.0. PFGR %65 01:14 Easy location |

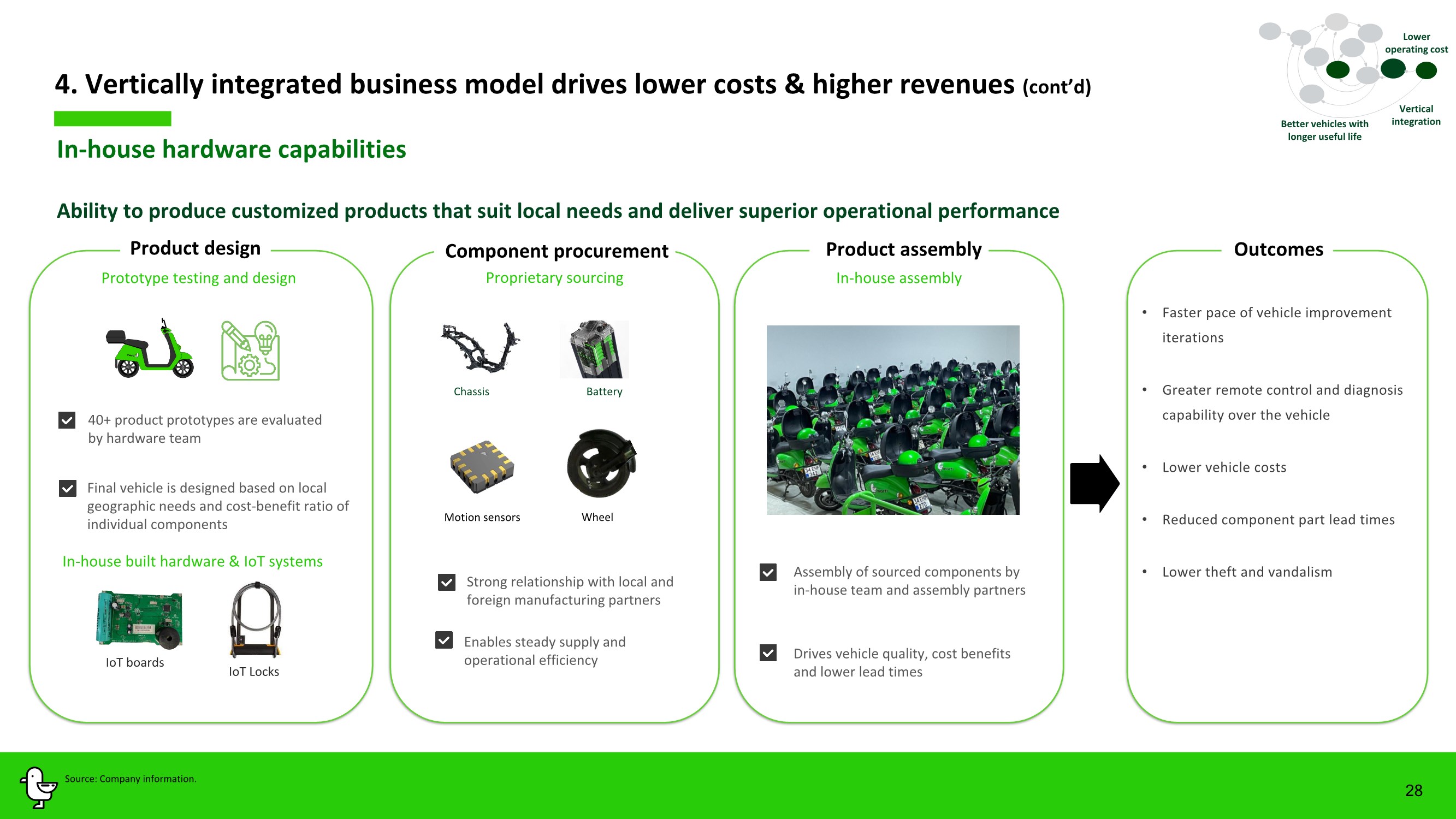

| 28 Ability to produce customized products that suit local needs and deliver superior operational performance In-house hardware capabilities Final vehicle is designed based on local geographic needs and cost-benefit ratio of individual components 40+ product prototypes are evaluated by hardware team Wheel Chassis Battery Motion sensors In-house built hardware & IoT systems IoT boards IoT Locks Strong relationship with local and foreign manufacturing partners Enables steady supply and operational efficiency Assembly of sourced components by in-house team and assembly partners Drives vehicle quality, cost benefits and lower lead times 4. Vertically integrated business model drives lower costs & higher revenues (cont’d) Vertical integration Better vehicles with longer useful life • Faster pace of vehicle improvement iterations • Greater remote control and diagnosis capability over the vehicle • Lower vehicle costs • Reduced component part lead times • Lower theft and vandalism Source: Company information. Lower operating cost Product assembly Product design Prototype testing and design Component procurement Outcomes Proprietary sourcing In-house assembly |

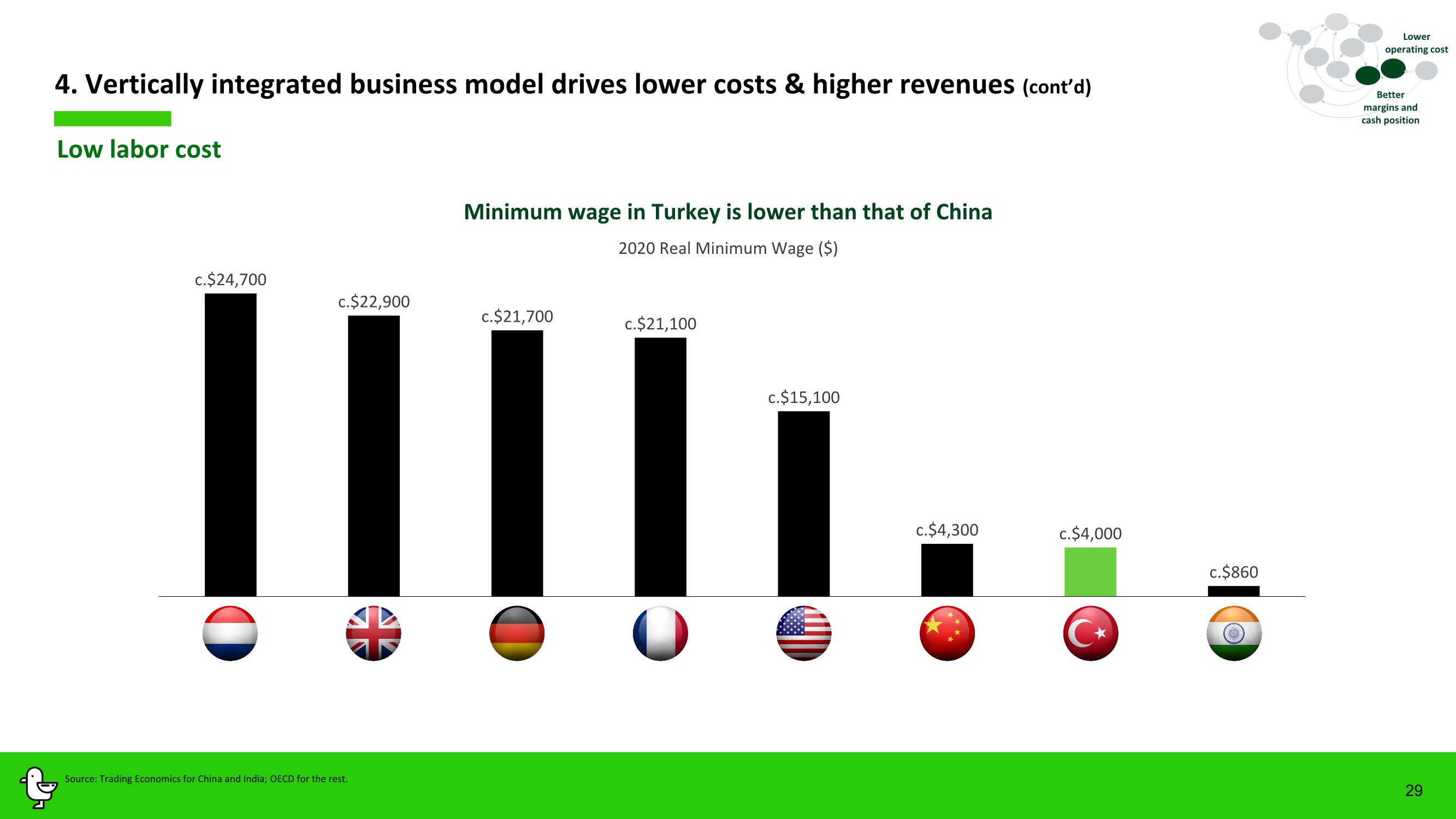

| 29 Low labor cost 4. Vertically integrated business model drives lower costs & higher revenues (cont’d) Better margins and cash position Source: Trading Economics for China and India; OECD for the rest. 2020 Real Minimum Wage ($) Minimum wage in Turkey is lower than that of China c.$24,700 c.$22,900 c.$21,700 c.$21,100 c.$15,100 c.$4,300 c.$4,000 c.$860 Lower operating cost |

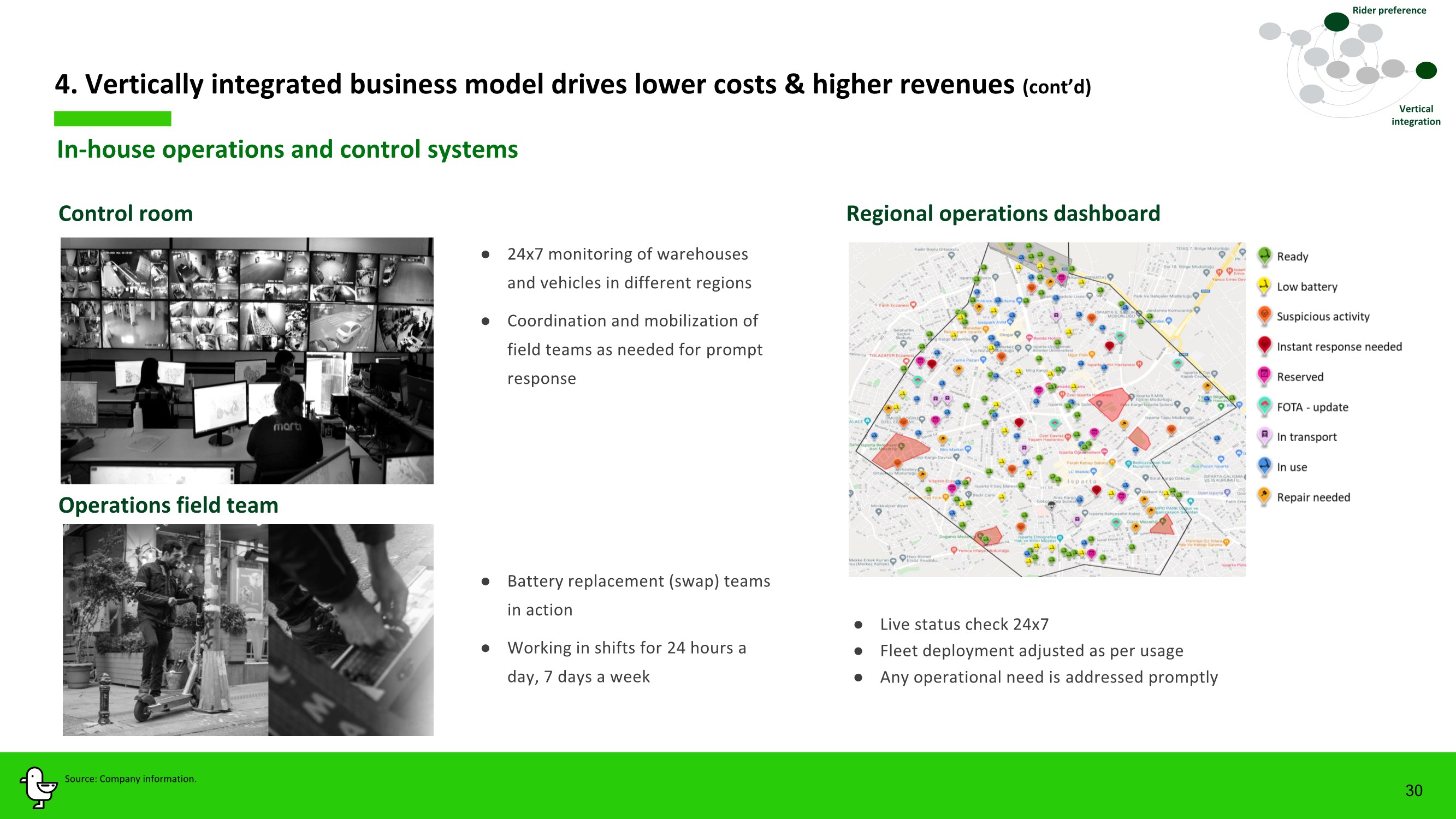

| Control room 30 ● Live status check 24x7 ● Fleet deployment adjusted as per usage ● Any operational need is addressed promptly ● 24x7 monitoring of warehouses and vehicles in different regions ● Coordination and mobilization of field teams as needed for prompt response ● Battery replacement (swap) teams in action ● Working in shifts for 24 hours a day, 7 days a week In-house operations and control systems Operations field team Regional operations dashboard 4. Vertically integrated business model drives lower costs & higher revenues (cont’d) Vertical integration Source: Company information. Rider preference |

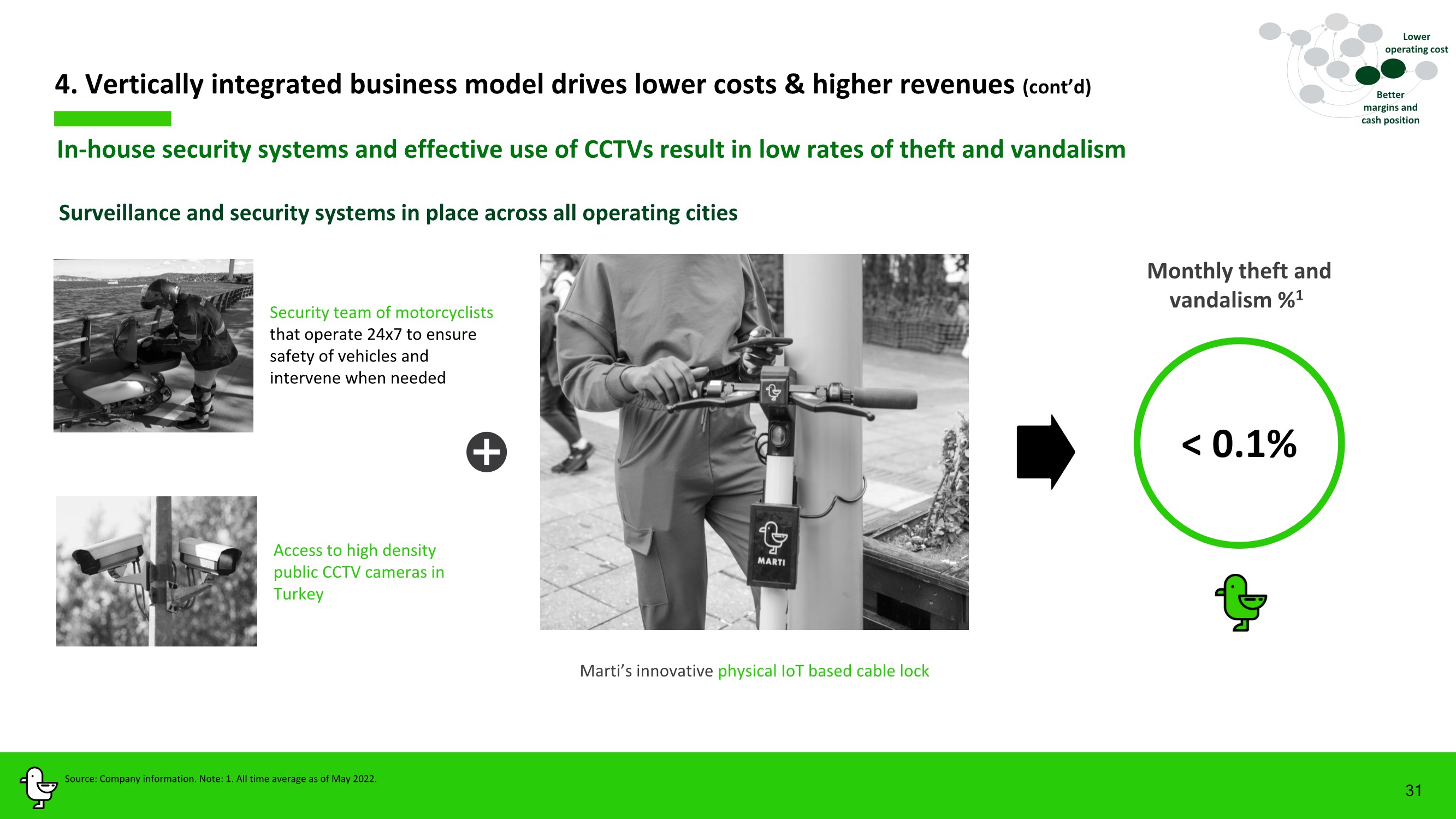

| In-house security systems and effective use of CCTVs result in low rates of theft and vandalism 4. Vertically integrated business model drives lower costs & higher revenues (cont’d) Surveillance and security systems in place across all operating cities 31 Marti’s innovative physical IoT based cable lock Security team of motorcyclists that operate 24x7 to ensure safety of vehicles and intervene when needed Access to high density public CCTV cameras in Turkey < 0.1% Better margins and cash position Source: Company information. Note: 1. All time average as of May 2022. Monthly theft and vandalism %1 Lower operating cost |

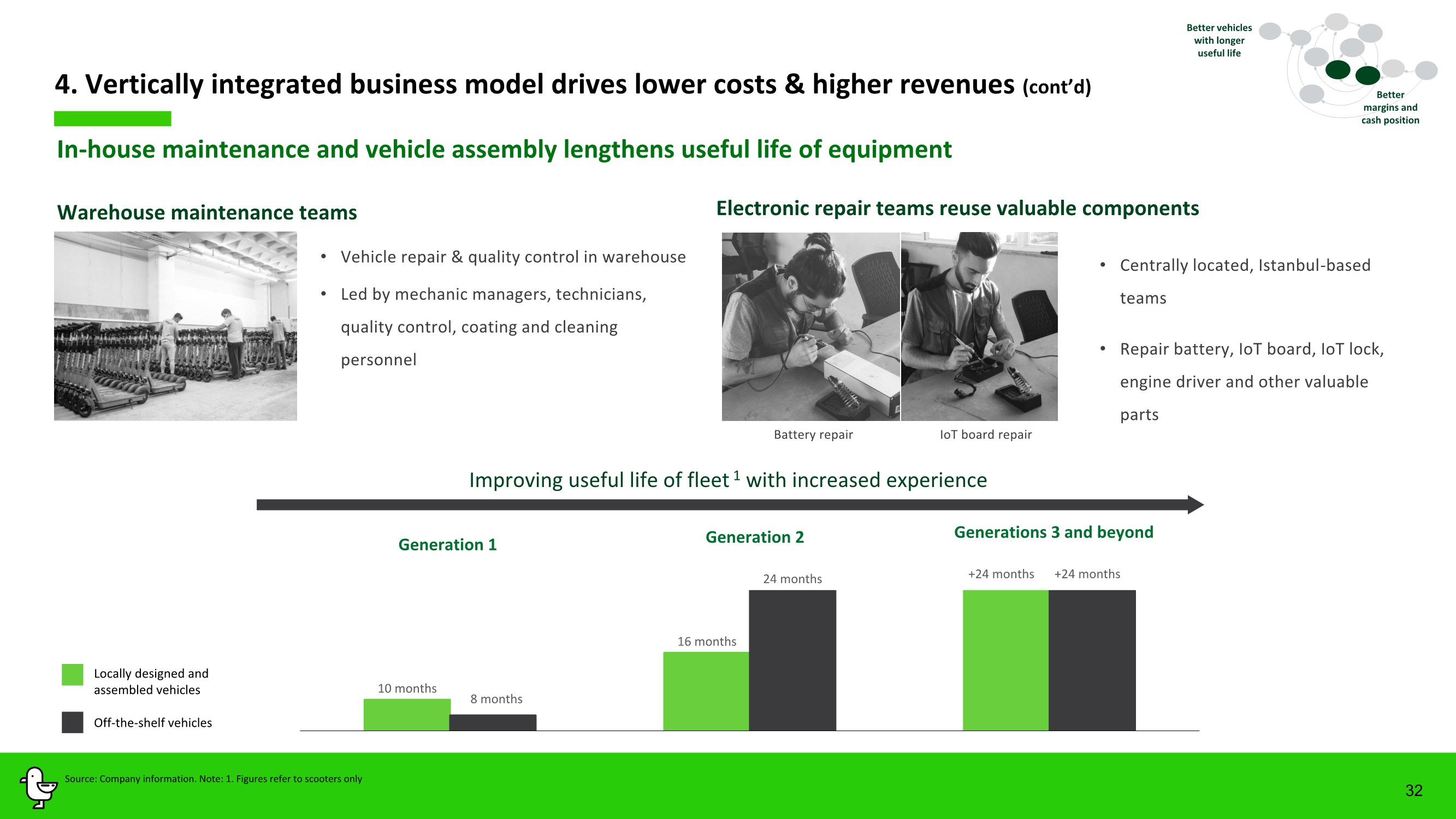

| • Centrally located, Istanbul-based teams • Repair battery, IoT board, IoT lock, engine driver and other valuable parts In-house maintenance and vehicle assembly lengthens useful life of equipment Electronic repair teams reuse valuable components 32 Warehouse maintenance teams • Vehicle repair & quality control in warehouse • Led by mechanic managers, technicians, quality control, coating and cleaning personnel Battery repair IoT board repair Improving useful life of fleet 1 with increased experience Better margins and cash position Generations 3 and beyond Generation 1 Generation 2 8 months +24 months +24 months Off-the-shelf vehicles 4. Vertically integrated business model drives lower costs & higher revenues (cont’d) Locally designed and assembled vehicles Better vehicles with longer useful life Source: Company information. Note: 1. Figures refer to scooters only 10 months 16 months 24 months |

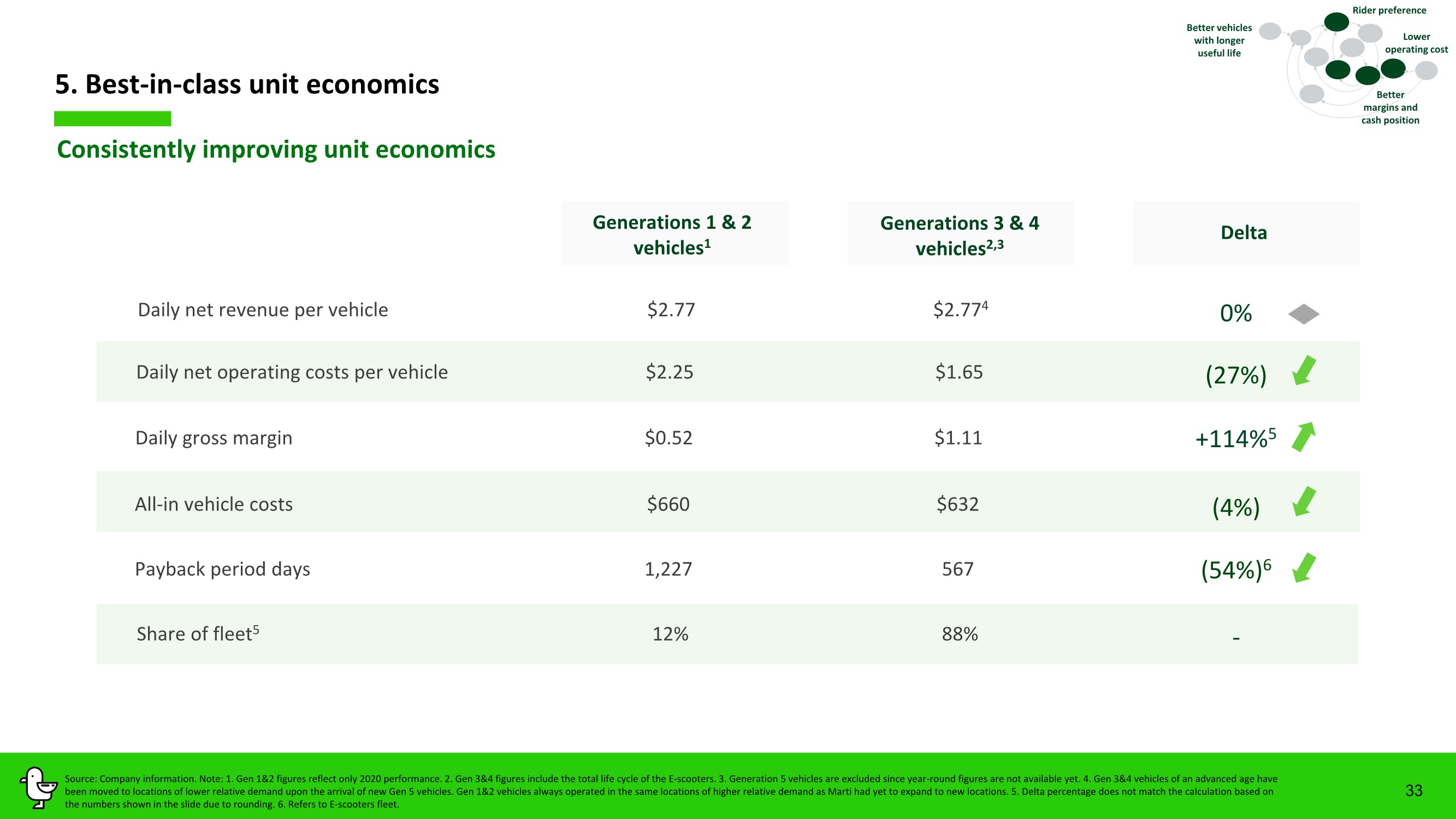

| 33 Consistently improving unit economics +114%5 Generations 3 & 4 vehicles2,3 Generations 1 & 2 vehicles1 Delta Daily net revenue per vehicle $2.77 $2.774 Daily net operating costs per vehicle $2.25 $1.65 Daily gross margin $0.52 $1.11 All-in vehicle costs $660 $632 Payback period days 1,227 567 Share of fleet5 12% 88% 0% (27%) (4%) (54%)6 - 5. Best-in-class unit economics Better vehicles with longer useful life Rider preference Source: Company information. Note: 1. Gen 1&2 figures reflect only 2020 performance. 2. Gen 3&4 figures include the total life cycle of the E-scooters. 3. Generation 5 vehicles are excluded since year-round figures are not available yet. 4. Gen 3&4 vehicles of an advanced age have been moved to locations of lower relative demand upon the arrival of new Gen 5 vehicles. Gen 1&2 vehicles always operated in the same locations of higher relative demand as Marti had yet to expand to new locations. 5. Delta percentage does not match the calculation based on the numbers shown in the slide due to rounding. 6. Refers to E-scooters fleet. Better margins and cash position Lower operating cost |

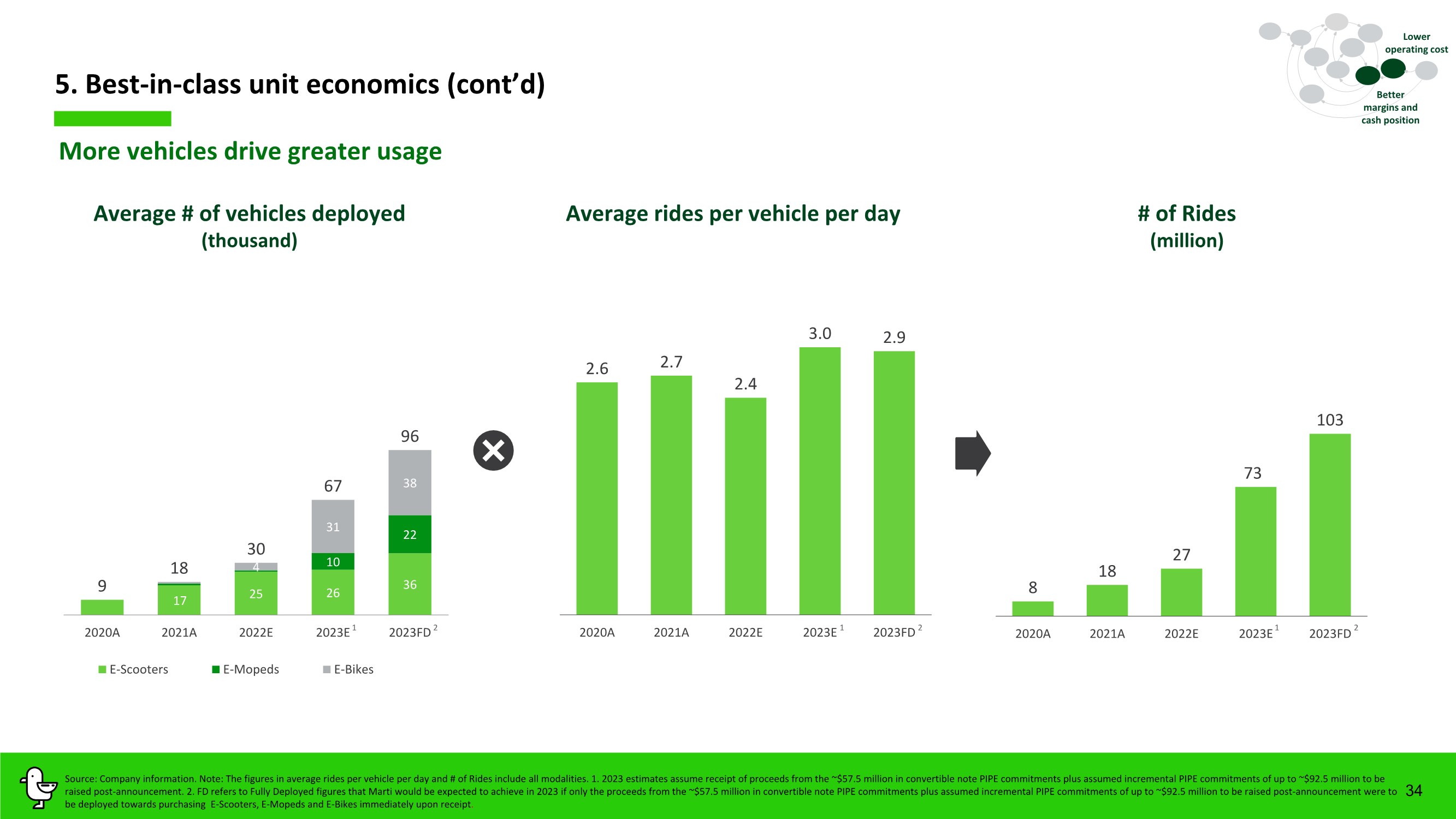

| 34 5. Best-in-class unit economics (cont’d) Average rides per vehicle per day Average # of vehicles deployed (thousand) # of Rides (million) More vehicles drive greater usage 17 25 26 36 10 22 4 31 38 9 18 30 67 96 2020A 2021A 2022E 2023E 2023FD E-Scooters E-Mopeds E-Bikes 8 18 27 73 103 2020A 2021A 2022E 2023E 2023FD 2.6 2.7 2.4 3.0 2.9 2020A 2021A 2022E 2023E 2023FD Source: Company information. Note: The figures in average rides per vehicle per day and # of Rides include all modalities. 1. 2023 estimates assume receipt of proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement. 2. FD refers to Fully Deployed figures that Marti would be expected to achieve in 2023 if only the proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement were to be deployed towards purchasing E-Scooters, E-Mopeds and E-Bikes immediately upon receipt. Lower operating cost Better margins and cash position 2 2 2 1 1 1 |

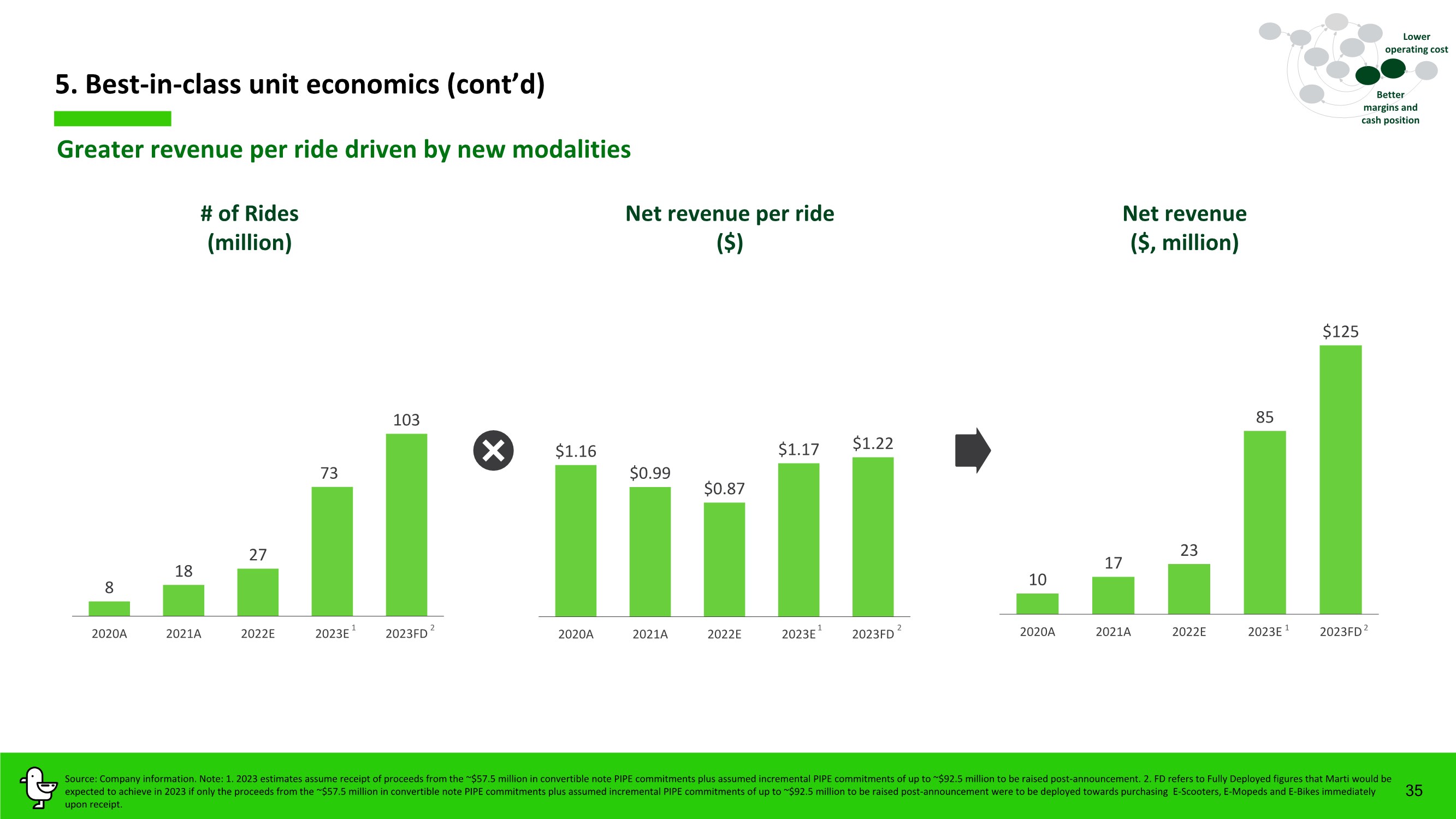

| 35 10 17 23 85 $125 2020A 2021A 2022E 2023E 2023FD Net revenue per ride ($) # of Rides (million) Net revenue ($, million) 5. Best-in-class unit economics (cont’d) Greater revenue per ride driven by new modalities Lower operating cost Source: Company information. Note: 1. 2023 estimates assume receipt of proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement. 2. FD refers to Fully Deployed figures that Marti would be expected to achieve in 2023 if only the proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement were to be deployed towards purchasing E-Scooters, E-Mopeds and E-Bikes immediately upon receipt. Better margins and cash position $1.16 $0.99 $0.87 $1.17 $1.22 2020A 2021A 2022E 2023E 2023FD 8 18 27 73 103 2020A 2021A 2022E 2023E 2023FD 2 2 2 1 1 1 |

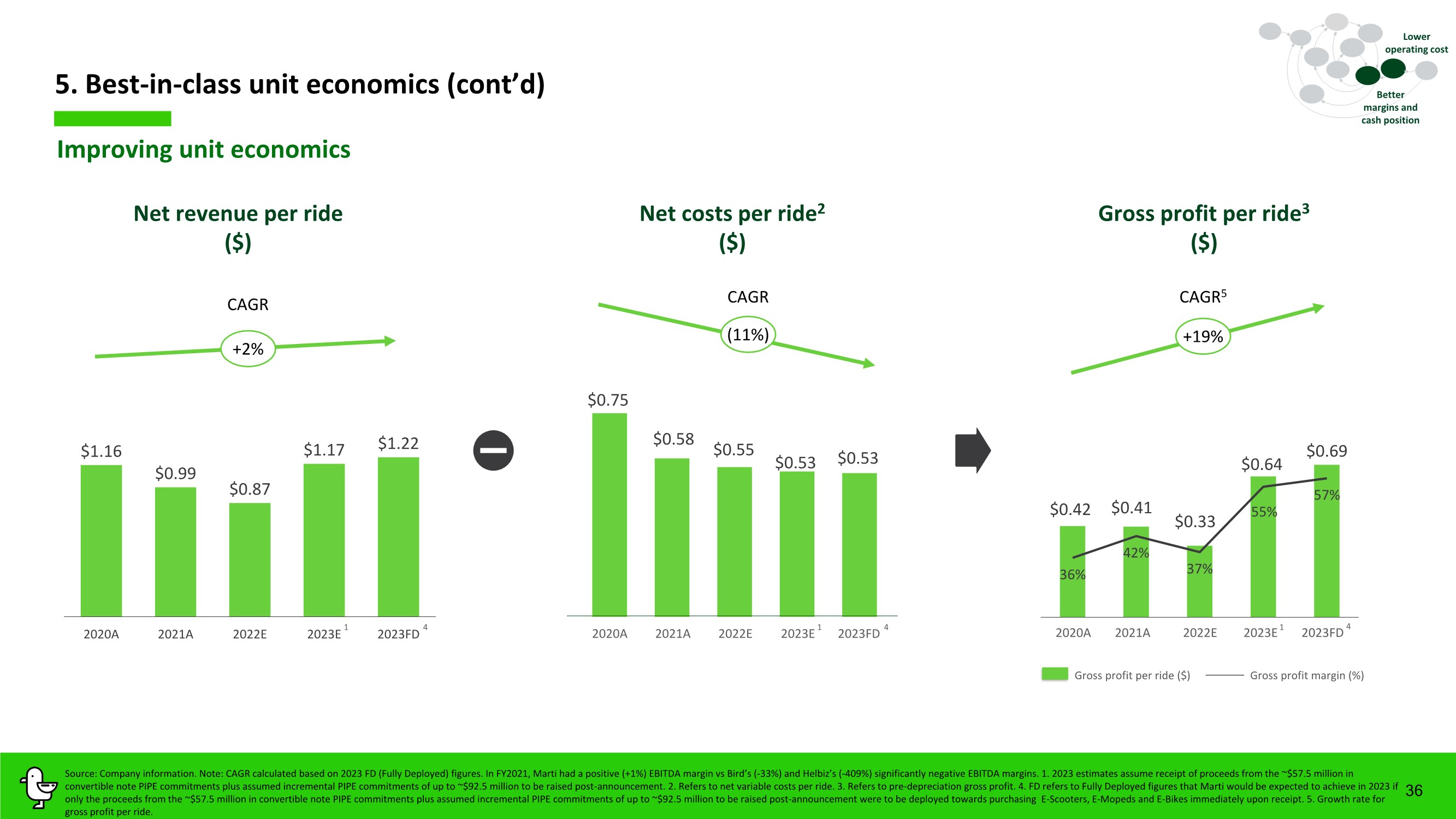

| $1.16 $0.99 $0.87 $1.17 $1.22 2020A 2021A 2022E 2023E 2023FD Net costs per ride2 ($) Net revenue per ride ($) Gross profit per ride3 ($) 5. Best-in-class unit economics (cont’d) 36 Improving unit economics Gross profit per ride ($) Gross profit margin (%) +2% CAGR 2020A 2021A 2022E 2023E 2023FD $0.42 $0.41 $0.33 $0.64 $0.69 36% 42% 37% 55% 57% $0.75 $0.58 $0.55 $0.53 $0.53 2020A 2021A 2022E 2023E Source: Company information. Note: CAGR calculated based on 2023 FD (Fully Deployed) figures. In FY2021, Marti had a positive (+1%) EBITDA margin vs Bird’s (-33%) and Helbiz’s (-409%) significantly negative EBITDA margins. 1. 2023 estimates assume receipt of proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement. 2. Refers to net variable costs per ride. 3. Refers to pre-depreciation gross profit. 4. FD refers to Fully Deployed figures that Marti would be expected to achieve in 2023 if only the proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement were to be deployed towards purchasing E-Scooters, E-Mopeds and E-Bikes immediately upon receipt. 5. Growth rate for gross profit per ride. (11%) CAGR +19% CAGR5 Lower operating cost Better margins and cash position 4 4 4 2023FD 1 1 1 |

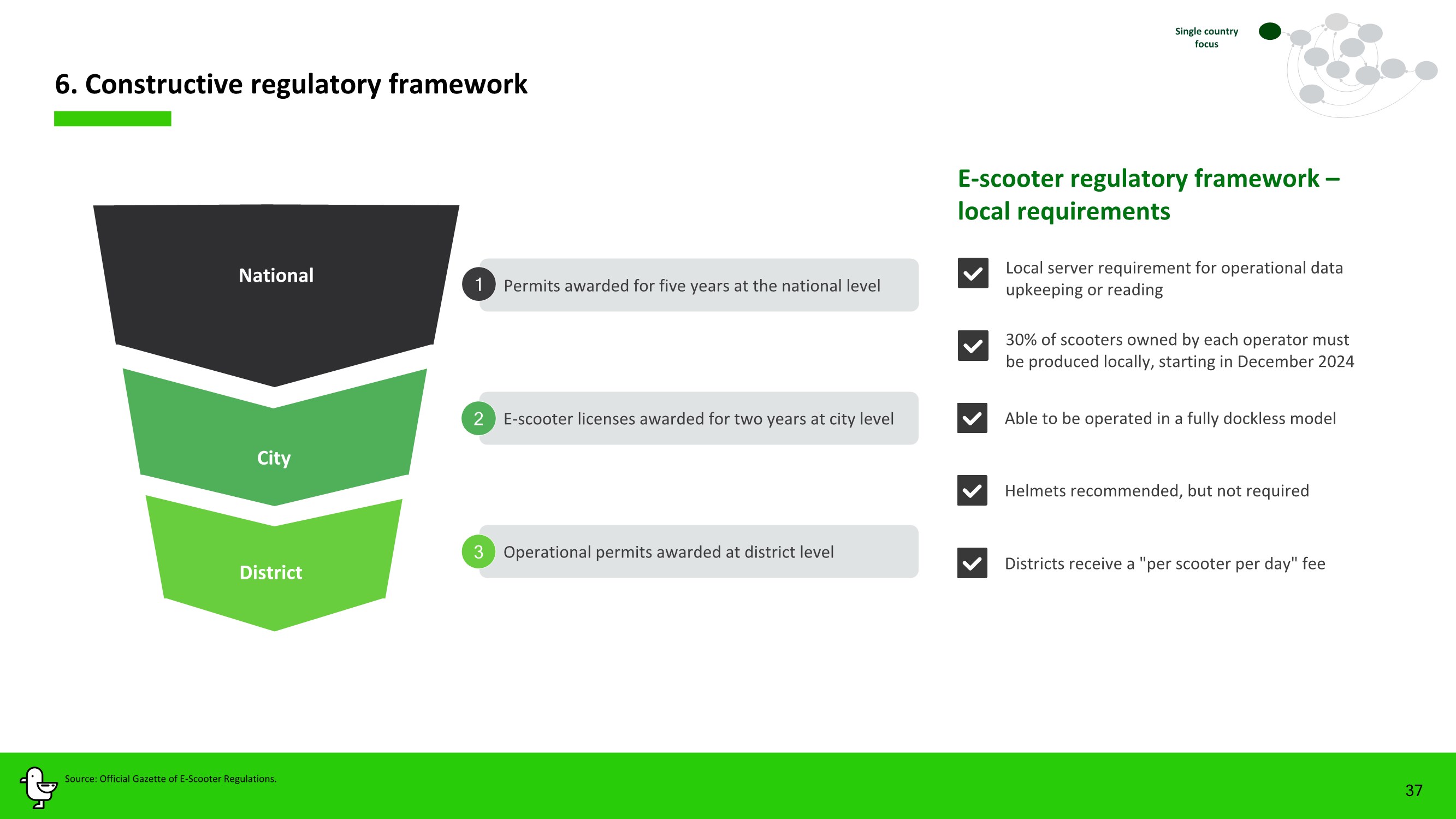

| 37 6. Constructive regulatory framework Operational permits awarded at district level E-scooter regulatory framework – local requirements 30% of scooters owned by each operator must be produced locally, starting in December 2024 Districts receive a "per scooter per day" fee Able to be operated in a fully dockless model Local server requirement for operational data upkeeping or reading Helmets recommended, but not required National City District E-scooter licenses awarded for two years at city level 2 3 Permits awarded for five years at the national level 1 Single country focus Source: Official Gazette of E-Scooter Regulations. |

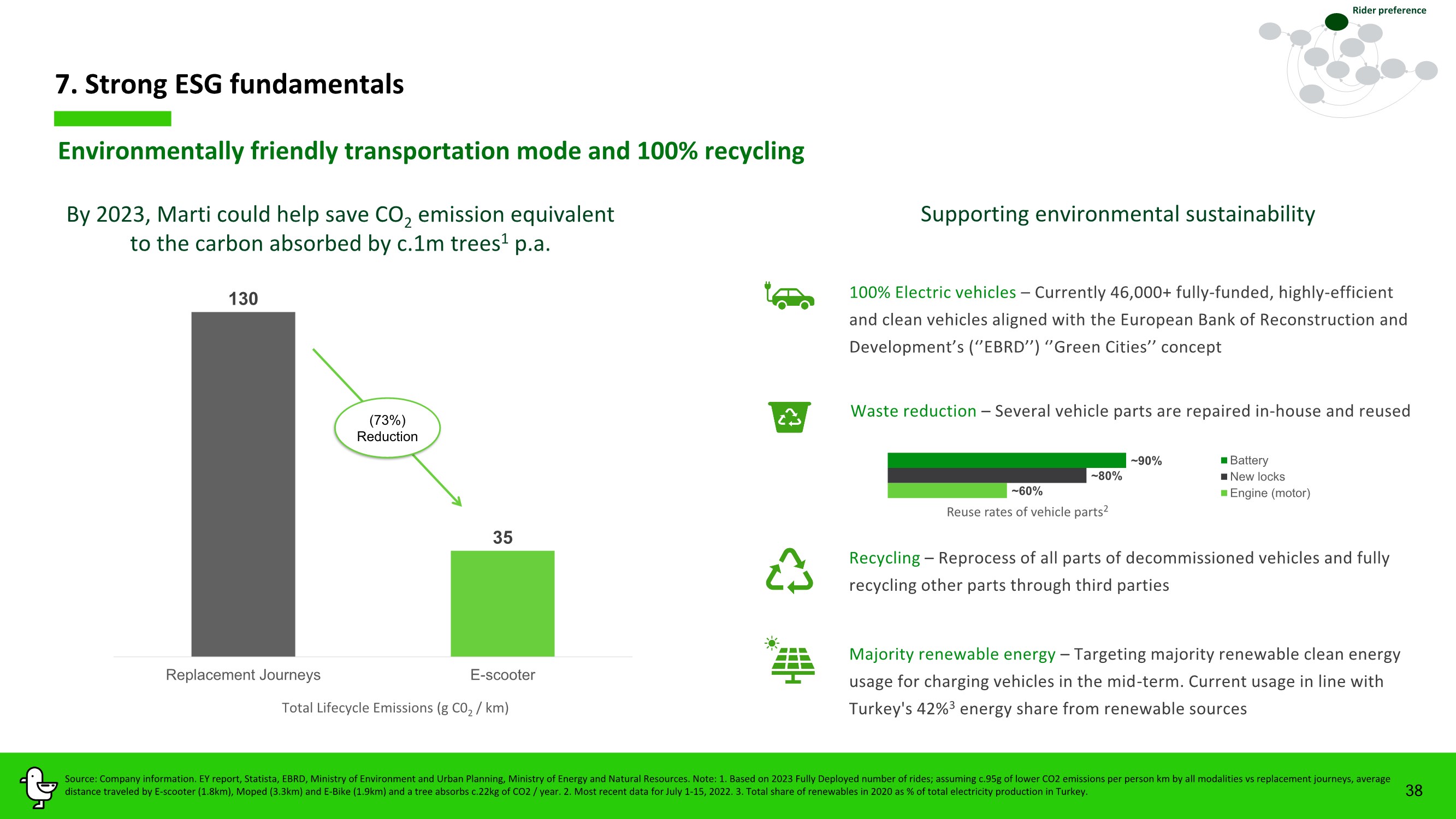

| 7. Strong ESG fundamentals 38 Environmentally friendly transportation mode and 100% recycling 130 35 Replacement Journeys E-scooter By 2023, Marti could help save CO2 emission equivalent to the carbon absorbed by c.1m trees1 p.a. Total Lifecycle Emissions (g C02 / km) (73%) Reduction Supporting environmental sustainability Recycling – Reprocess of all parts of decommissioned vehicles and fully recycling other parts through third parties Waste reduction – Several vehicle parts are repaired in-house and reused 100% Electric vehicles – Currently 46,000+ fully-funded, highly-efficient and clean vehicles aligned with the European Bank of Reconstruction and Development’s (‘’EBRD’’) ‘’Green Cities’’ concept Majority renewable energy – Targeting majority renewable clean energy usage for charging vehicles in the mid-term. Current usage in line with Turkey's 42%3 energy share from renewable sources ~60% ~80% ~90% Battery New locks Engine (motor) Reuse rates of vehicle parts2 Source: Company information. EY report, Statista, EBRD, Ministry of Environment and Urban Planning, Ministry of Energy and Natural Resources. Note: 1. Based on 2023 Fully Deployed number of rides; assuming c.95g of lower CO2 emissions per person km by all modalities vs replacement journeys, average distance traveled by E-scooter (1.8km), Moped (3.3km) and E-Bike (1.9km) and a tree absorbs c.22kg of CO2 / year. 2. Most recent data for July 1-15, 2022. 3. Total share of renewables in 2020 as % of total electricity production in Turkey. Rider preference |

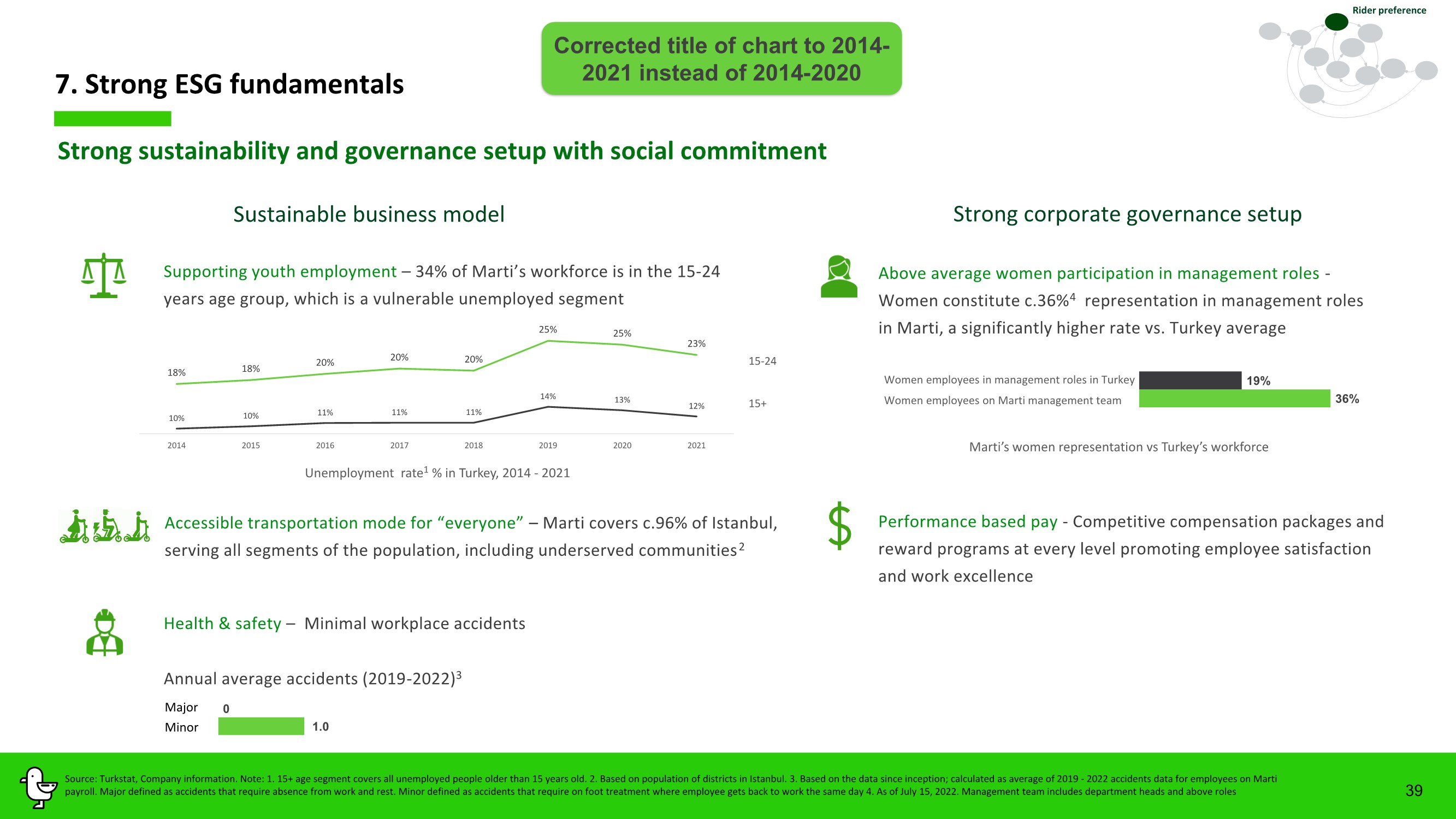

| Major 7. Strong ESG fundamentals 39 Strong sustainability and governance setup with social commitment Sustainable business model Strong corporate governance setup Supporting youth employment – 34% of Marti’s workforce is in the 15-24 years age group, which is a vulnerable unemployed segment Accessible transportation mode for “everyone” – Marti covers c.96% of Istanbul, serving all segments of the population, including underserved communities2 Performance based pay - Competitive compensation packages and reward programs at every level promoting employee satisfaction and work excellence 36% 19% Above average women participation in management roles - Women constitute c.36%4 representation in management roles in Marti, a significantly higher rate vs. Turkey average Health & safety – Minimal workplace accidents Unemployment rate1 % in Turkey, 2014 - 2021 Marti’s women representation vs Turkey’s workforce 1.0 0 Minor Annual average accidents (2019-2022)3 15+ 15-24 Women employees in management roles in Turkey Women employees on Marti management team Source: Turkstat, Company information. Note: 1. 15+ age segment covers all unemployed people older than 15 years old. 2. Based on population of districts in Istanbul. 3. Based on the data since inception; calculated as average of 2019 - 2022 accidents data for employees on Marti payroll. Major defined as accidents that require absence from work and rest. Minor defined as accidents that require on foot treatment where employee gets back to work the same day 4. As of July 15, 2022. Management team includes department heads and above roles Rider preference 18% 18% 20% 20% 20% 25% 25% 23% 10% 10% 11% 11% 11% 14% 13% 12% 2014 2015 2016 2017 2018 2019 2020 2021 Corrected title of chart to 2014- 2021 instead of 2014-2020 |

| Financials |

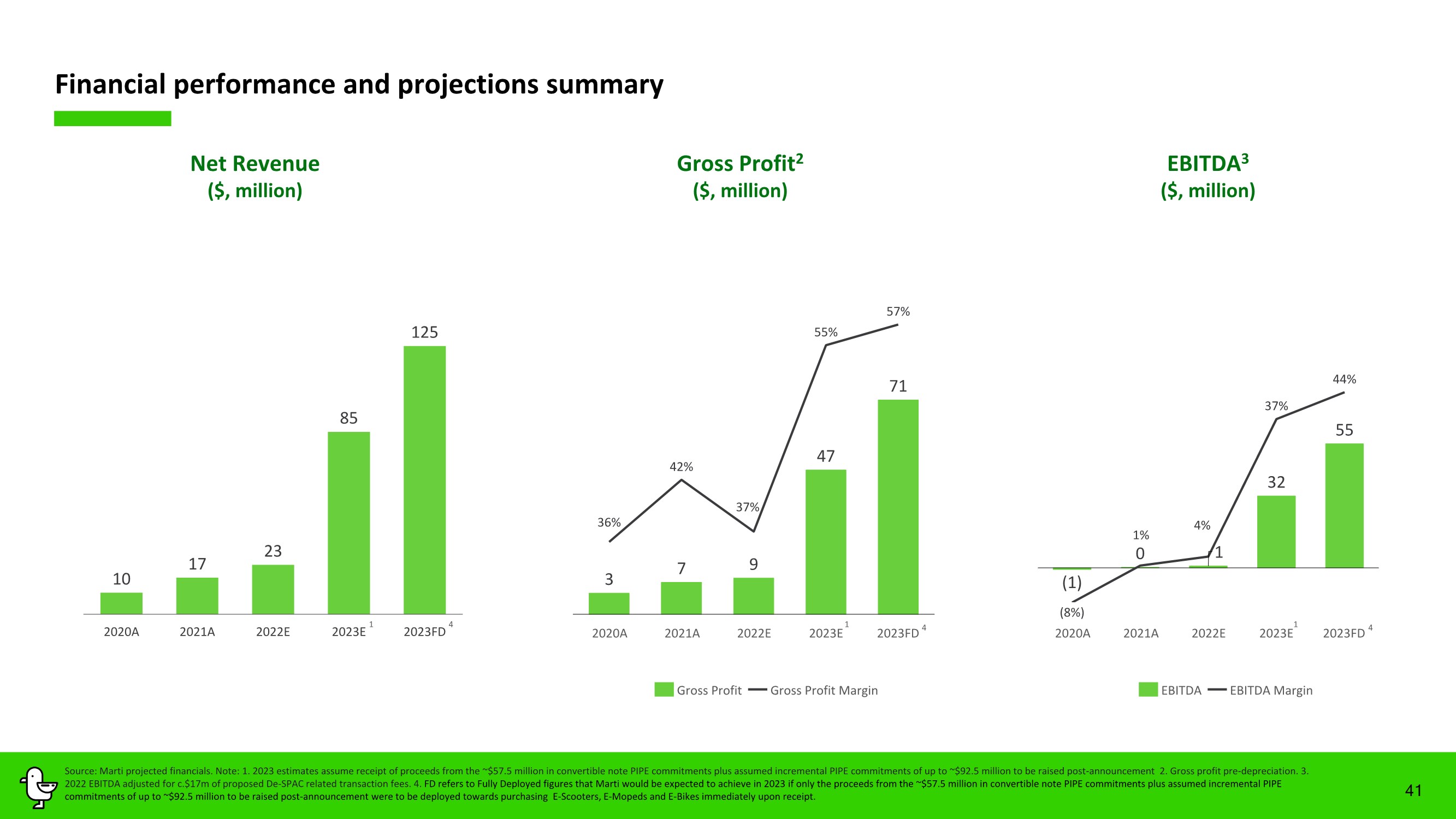

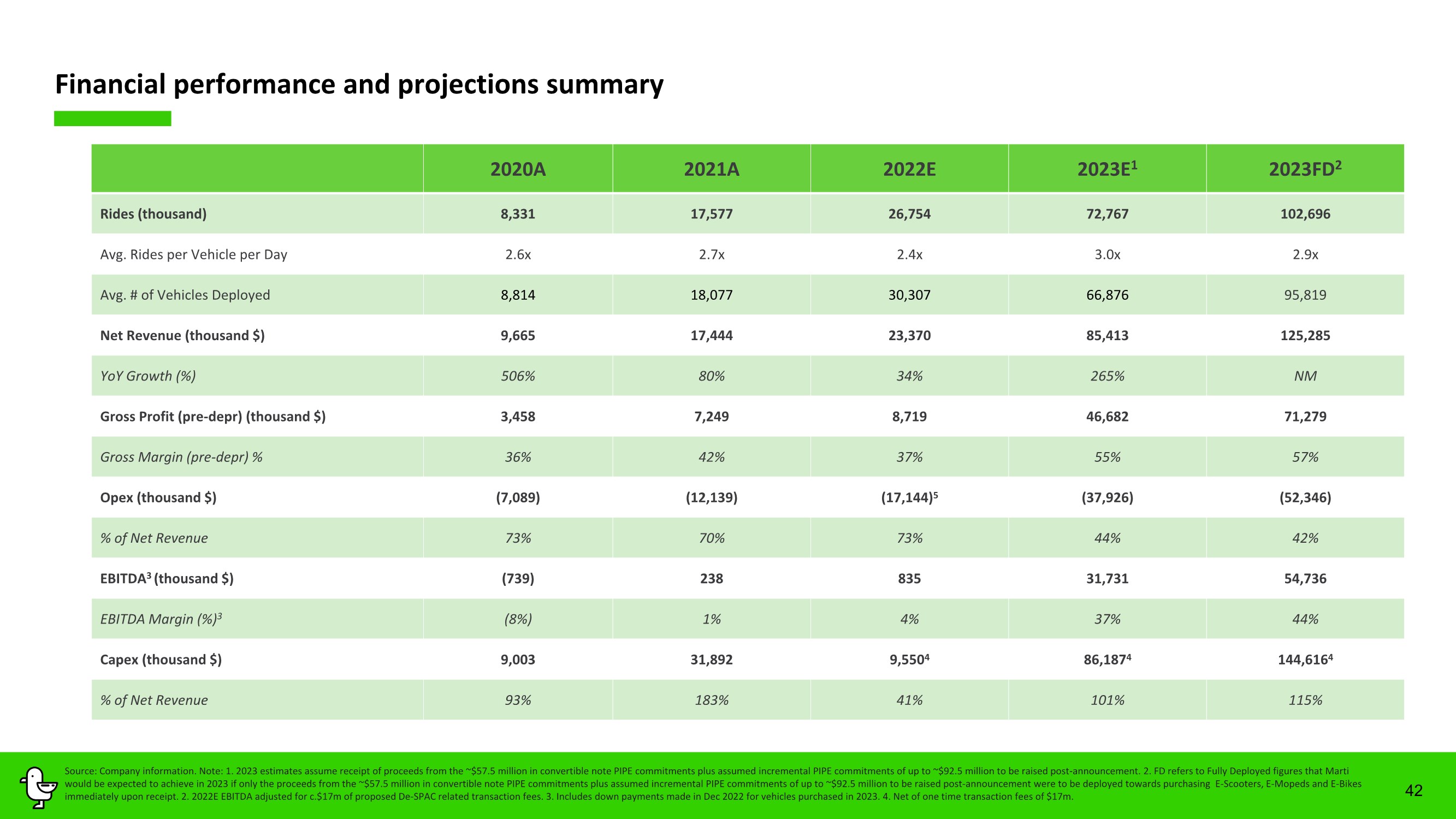

| 41 EBITDA3 ($, million) Gross Profit2 ($, million) Financial performance and projections summary Net Revenue ($, million) (1) 0 1 32 55 (8%) 1% 4% 37% 44% -8% -15 35 85 EBITDA EBITDA Margin 3 7 9 47 71 36% 42% 37% 55% 57% 29% 34% 39% 44% 49% 54% 59% -4 46 96 Gross Profit Gross Profit Margin Source: Marti projected financials. Note: 1. 2023 estimates assume receipt of proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement 2. Gross profit pre-depreciation. 3. 2022 EBITDA adjusted for c.$17m of proposed De-SPAC related transaction fees. 4. FD refers to Fully Deployed figures that Marti would be expected to achieve in 2023 if only the proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement were to be deployed towards purchasing E-Scooters, E-Mopeds and E-Bikes immediately upon receipt. 10 17 23 85 125 2020A 2021A 2022E 2023E 2023FD 2020A 2021A 2022E 2023E 2023FD 2020A 2021A 2022E 2023E 2023FD 4 4 4 1 1 1 |

| 42 2020A 2021A 2022E 2023E1 2023FD2 Rides (thousand) 8,331 17,577 26,754 72,767 102,696 Avg. Rides per Vehicle per Day 2.6x 2.7x 2.4x 3.0x 2.9x Avg. # of Vehicles Deployed 8,814 18,077 30,307 66,876 95,819 Net Revenue (thousand $) 9,665 17,444 23,370 85,413 125,285 YoY Growth (%) 506% 80% 34% 265% NM Gross Profit (pre-depr) (thousand $) 3,458 7,249 8,719 46,682 71,279 Gross Margin (pre-depr) % 36% 42% 37% 55% 57% Opex (thousand $) (7,089) (12,139) (17,144)5 (37,926) (52,346) % of Net Revenue 73% 70% 73% 44% 42% EBITDA3 (thousand $) (739) 238 835 31,731 54,736 EBITDA Margin (%)3 (8%) 1% 4% 37% 44% Capex (thousand $) 9,003 31,892 9,5504 86,1874 144,6164 % of Net Revenue 93% 183% 41% 101% 115% Financial performance and projections summary Source: Company information. Note: 1. 2023 estimates assume receipt of proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement. 2. FD refers to Fully Deployed figures that Marti would be expected to achieve in 2023 if only the proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement were to be deployed towards purchasing E-Scooters, E-Mopeds and E-Bikes immediately upon receipt. 2. 2022E EBITDA adjusted for c.$17m of proposed De-SPAC related transaction fees. 3. Includes down payments made in Dec 2022 for vehicles purchased in 2023. 4. Net of one time transaction fees of $17m. |

| Transaction Summary |

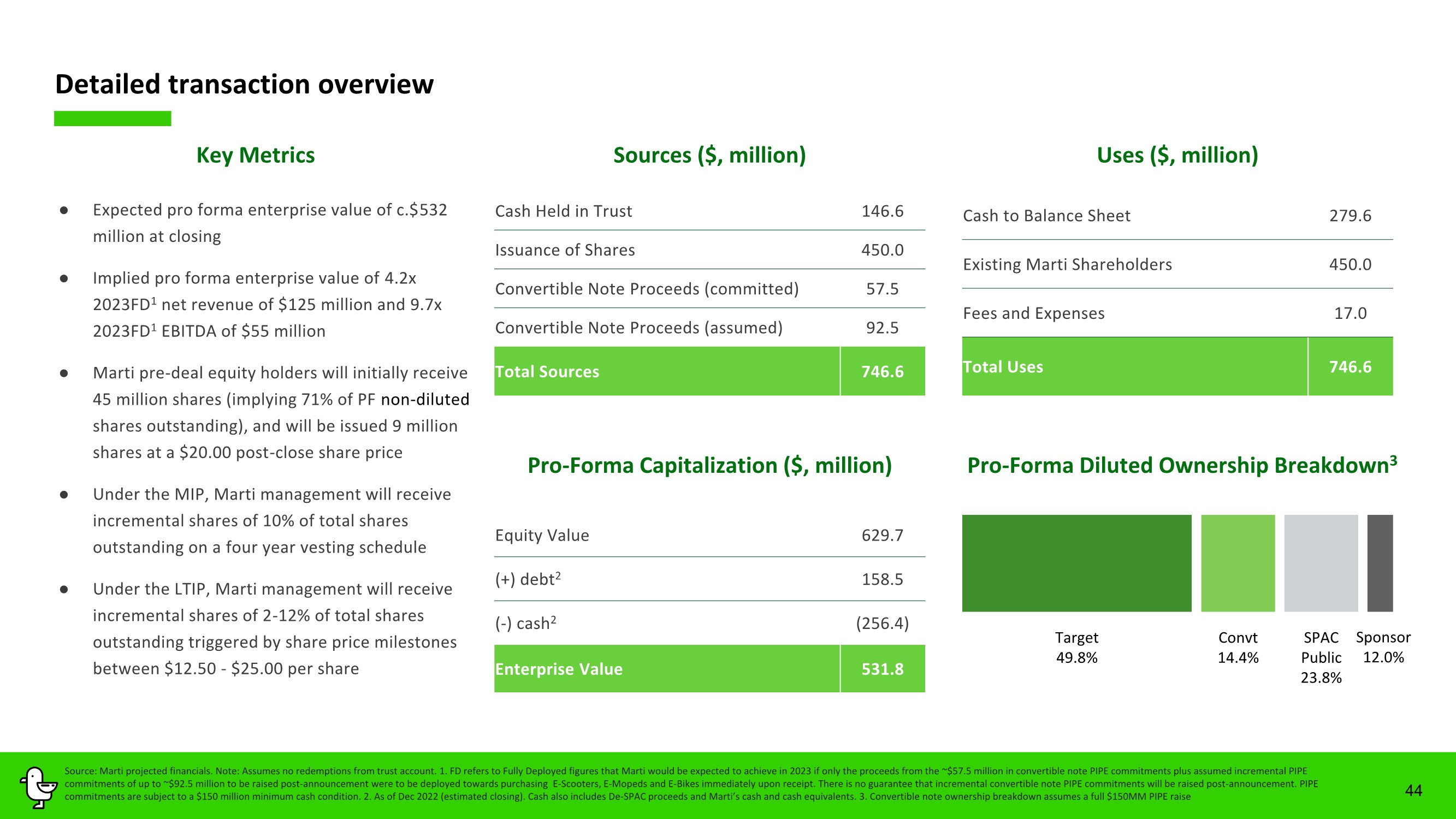

| Detailed transaction overview Sources ($, million) Uses ($, million) 44 Pro-Forma Diluted Ownership Breakdown3 Key Metrics ● Expected pro forma enterprise value of c.$532 million at closing ● Implied pro forma enterprise value of 4.2x 2023FD1 net revenue of $125 million and 9.7x 2023FD1 EBITDA of $55 million ● Marti pre-deal equity holders will initially receive 45 million shares (implying 71% of PF non-diluted shares outstanding), and will be issued 9 million shares at a $20.00 post-close share price ● Under the MIP, Marti management will receive incremental shares of 10% of total shares outstanding on a four year vesting schedule ● Under the LTIP, Marti management will receive incremental shares of 2-12% of total shares outstanding triggered by share price milestones between $12.50 - $25.00 per share Cash to Balance Sheet 279.6 Existing Marti Shareholders 450.0 Fees and Expenses 17.0 Total Uses 746.6 Cash Held in Trust 146.6 Issuance of Shares 450.0 Convertible Note Proceeds (committed) 57.5 Convertible Note Proceeds (assumed) 92.5 Total Sources 746.6 Target 49.8% Sponsor 12.0% Convt 14.4% SPAC Public 23.8% Pro-Forma Capitalization ($, million) Equity Value 629.7 (+) debt2 158.5 (-) cash2 (256.4) Enterprise Value 531.8 Source: Marti projected financials. Note: Assumes no redemptions from trust account. 1. FD refers to Fully Deployed figures that Marti would be expected to achieve in 2023 if only the proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement were to be deployed towards purchasing E-Scooters, E-Mopeds and E-Bikes immediately upon receipt. There is no guarantee that incremental convertible note PIPE commitments will be raised post-announcement. PIPE commitments are subject to a $150 million minimum cash condition. 2. As of Dec 2022 (estimated closing). Cash also includes De-SPAC proceeds and Marti’s cash and cash equivalents. 3. Convertible note ownership breakdown assumes a full $150MM PIPE raise |

| Appendix |

| Comparable peers overview 46 Micro-mobility …and our journey could take us here Mobility super app We are here today… |

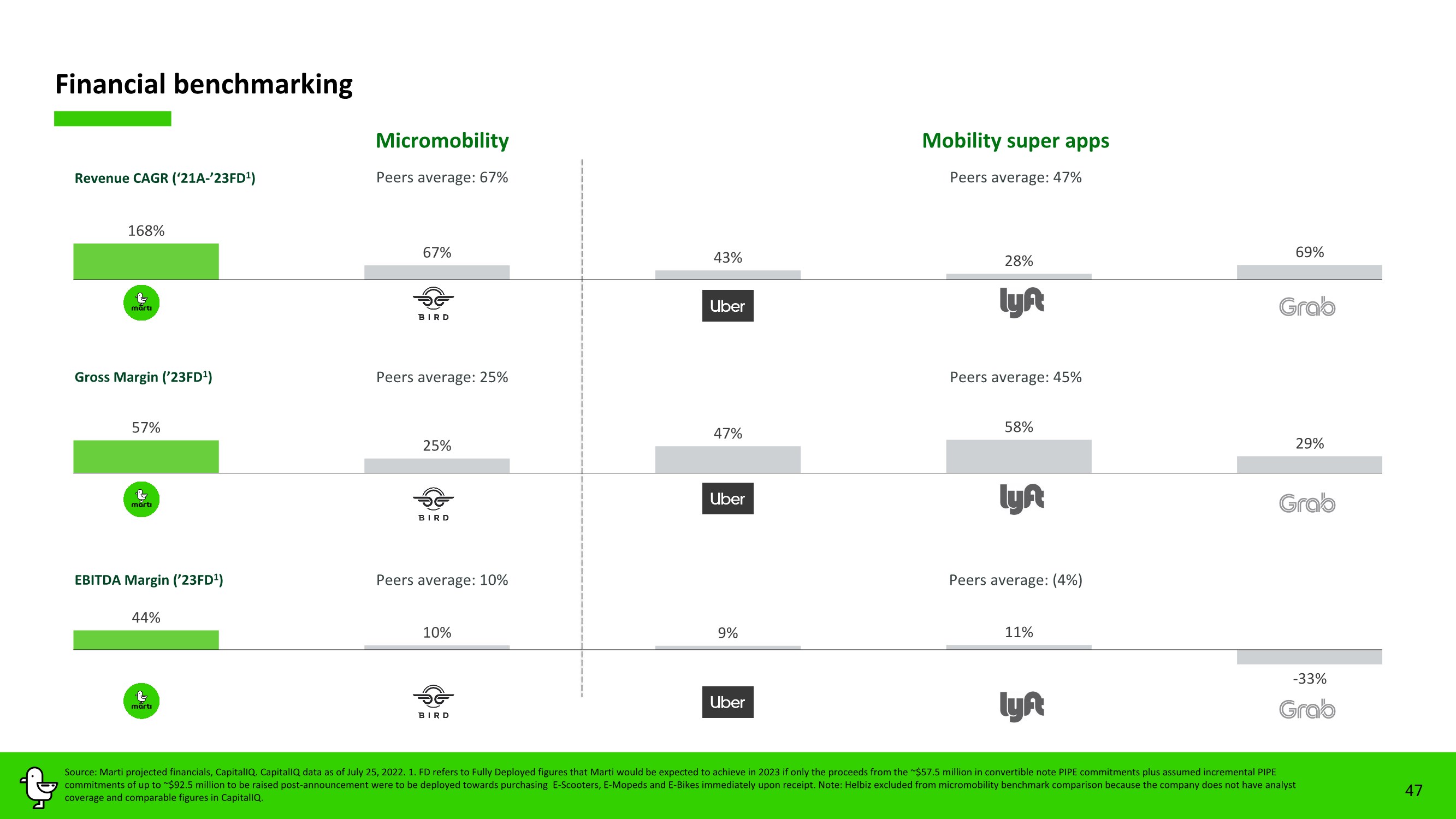

| 57% 25% 47% 58% 29% 168% 67% 43% 28% 69% Financial benchmarking Micromobility 47 Mobility super apps Revenue CAGR (‘21A-’23FD1) Gross Margin (’23FD1) Peers average: 25% Peers average: 67% Source: Marti projected financials, CapitalIQ. CapitalIQ data as of July 25, 2022. 1. FD refers to Fully Deployed figures that Marti would be expected to achieve in 2023 if only the proceeds from the ~$57.5 million in convertible note PIPE commitments plus assumed incremental PIPE commitments of up to ~$92.5 million to be raised post-announcement were to be deployed towards purchasing E-Scooters, E-Mopeds and E-Bikes immediately upon receipt. Note: Helbiz excluded from micromobility benchmark comparison because the company does not have analyst coverage and comparable figures in CapitalIQ. 44% 10% 9% 11% -33% Peers average: 47% Peers average: 45% EBITDA Margin (’23FD1) Peers average: 10% Peers average: (4%) |

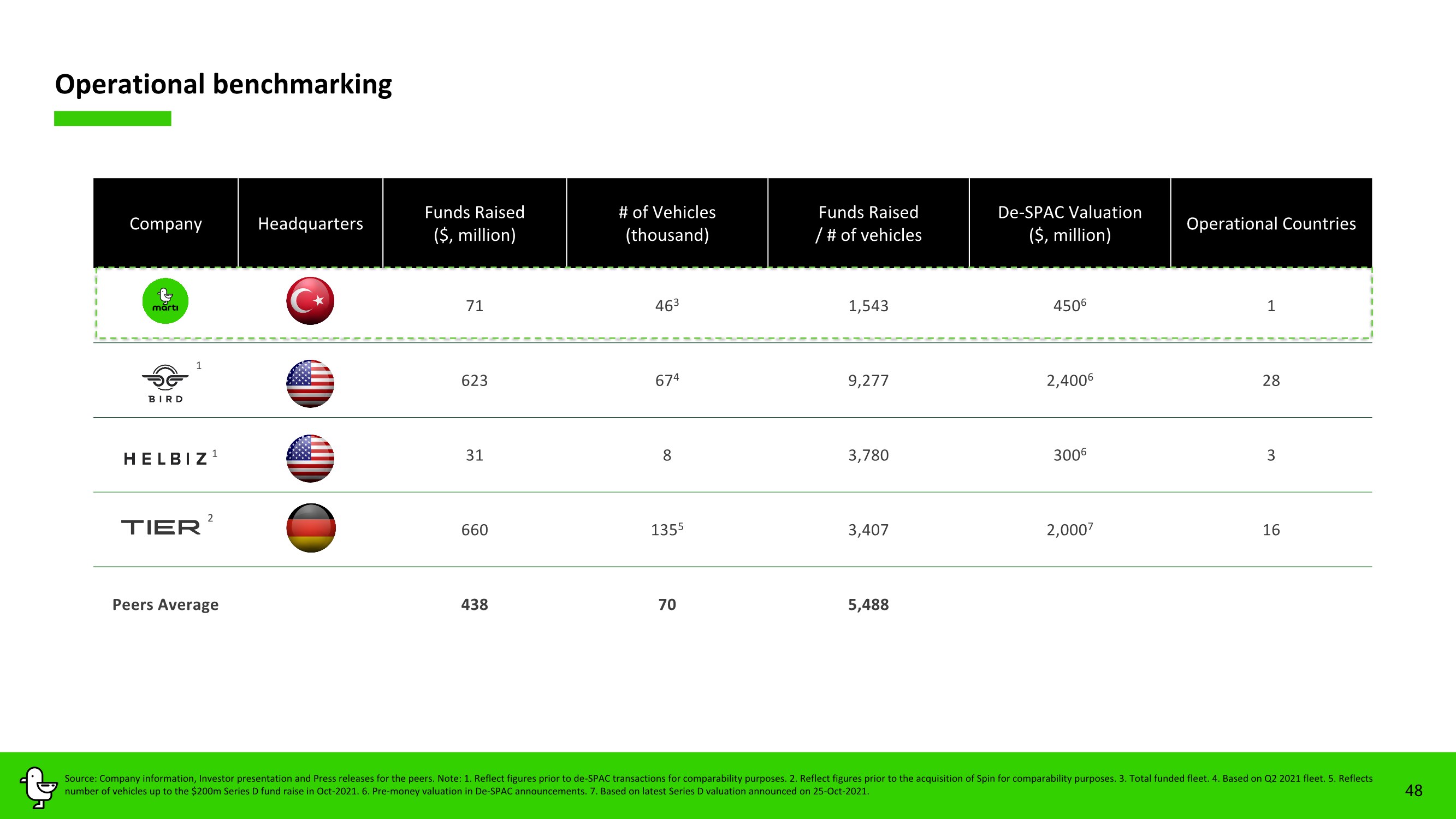

| 48 Operational benchmarking Company Headquarters Funds Raised ($, million) # of Vehicles (thousand) Funds Raised / # of vehicles De-SPAC Valuation ($, million) Operational Countries 71 463 1,543 4506 1 623 674 9,277 2,4006 28 31 8 3,780 3006 3 660 1355 3,407 2,0007 16 Peers Average 438 70 5,488 Source: Company information, Investor presentation and Press releases for the peers. Note: 1. Reflect figures prior to de-SPAC transactions for comparability purposes. 2. Reflect figures prior to the acquisition of Spin for comparability purposes. 3. Total funded fleet. 4. Based on Q2 2021 fleet. 5. Reflects number of vehicles up to the $200m Series D fund raise in Oct-2021. 6. Pre-money valuation in De-SPAC announcements. 7. Based on latest Series D valuation announced on 25-Oct-2021. 1 1 2 |

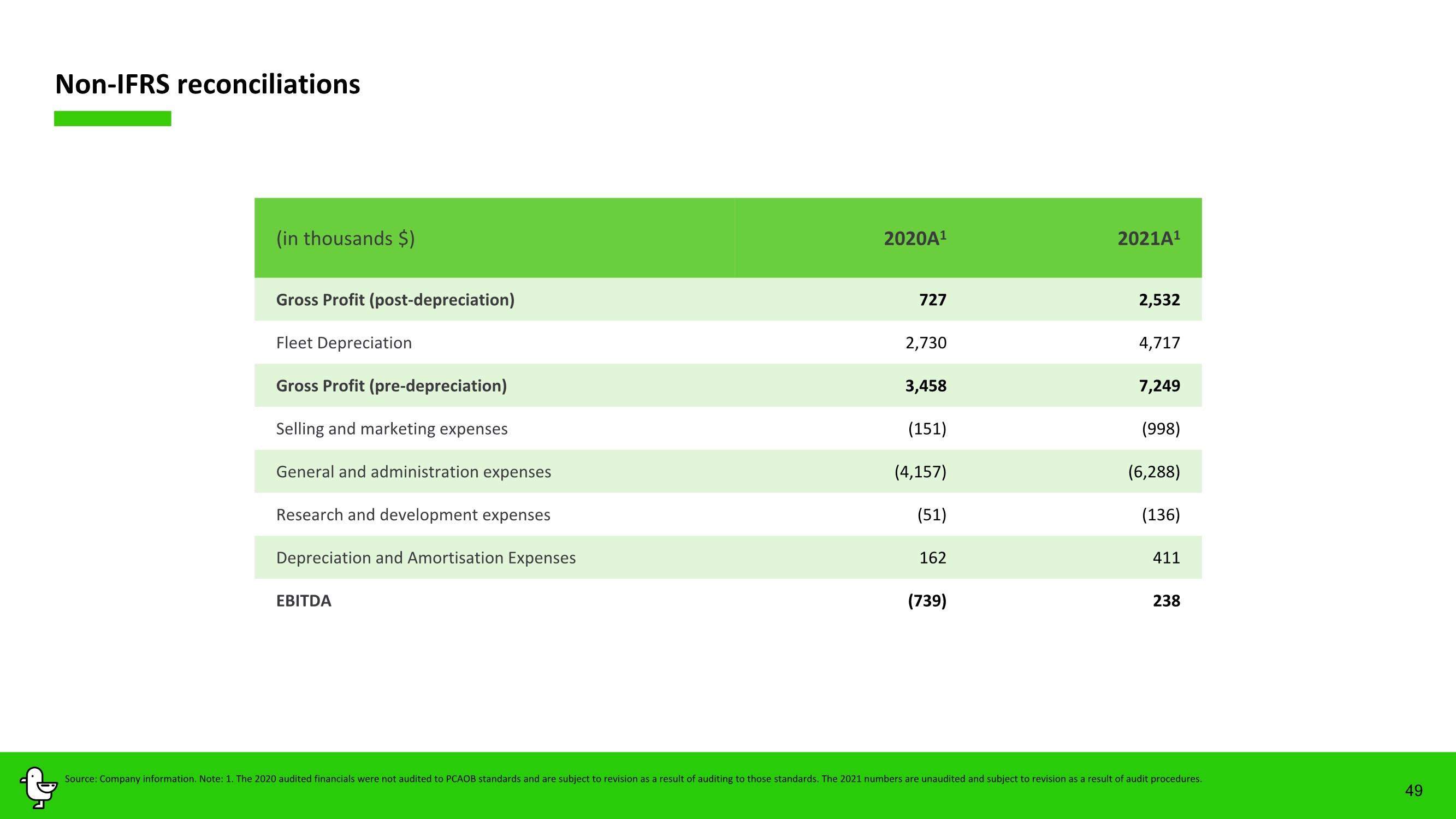

| 49 Non-IFRS reconciliations (in thousands $) 2020A1 2021A1 Gross Profit (post-depreciation) 727 2,532 Fleet Depreciation 2,730 4,717 Gross Profit (pre-depreciation) 3,458 7,249 Selling and marketing expenses (151) (998) General and administration expenses (4,157) (6,288) Research and development expenses (51) (136) Depreciation and Amortisation Expenses 162 411 EBITDA (739) 238 Source: Company information. Note: 1. The 2020 audited financials were not audited to PCAOB standards and are subject to revision as a result of auditing to those standards. The 2021 numbers are unaudited and subject to revision as a result of audit procedures. |

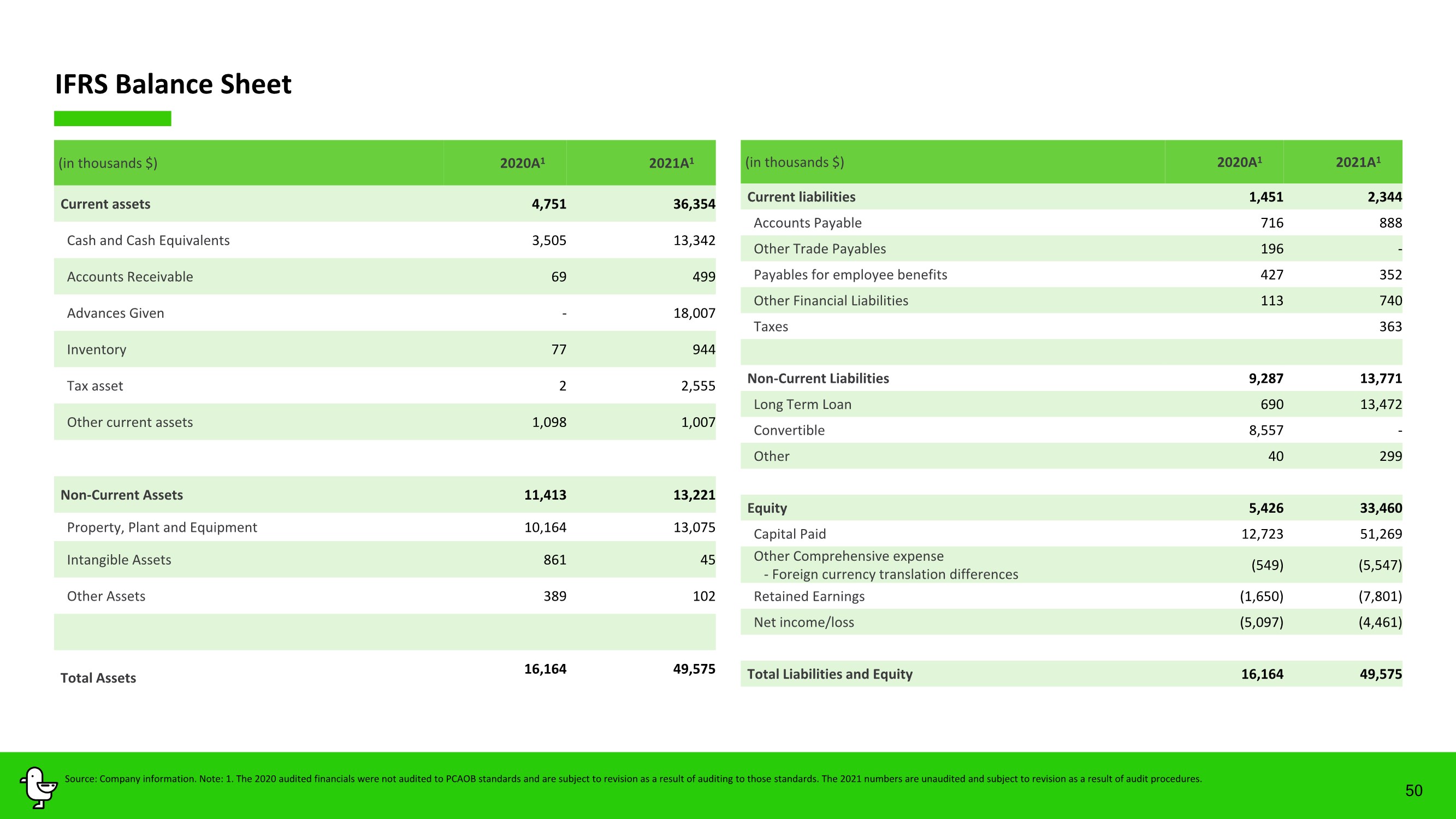

| 50 IFRS Balance Sheet (in thousands $) 2020A1 2021A1 Current assets 4,751 36,354 Cash and Cash Equivalents 3,505 13,342 Accounts Receivable 69 499 Advances Given - 18,007 Inventory 77 944 Tax asset 2 2,555 Other current assets 1,098 1,007 Non-Current Assets 11,413 13,221 Property, Plant and Equipment 10,164 13,075 Intangible Assets 861 45 Other Assets 389 102 Total Assets 16,164 49,575 (in thousands $) 2020A1 2021A1 Current liabilities 1,451 2,344 Accounts Payable 716 888 Other Trade Payables 196 - Payables for employee benefits 427 352 Other Financial Liabilities 113 740 Taxes 363 Non-Current Liabilities 9,287 13,771 Long Term Loan 690 13,472 Convertible 8,557 - Other 40 299 Equity 5,426 33,460 Capital Paid 12,723 51,269 Other Comprehensive expense - Foreign currency translation differences (549) (5,547) Retained Earnings (1,650) (7,801) Net income/loss (5,097) (4,461) Total Liabilities and Equity 16,164 49,575 Source: Company information. Note: 1. The 2020 audited financials were not audited to PCAOB standards and are subject to revision as a result of auditing to those standards. The 2021 numbers are unaudited and subject to revision as a result of audit procedures. |

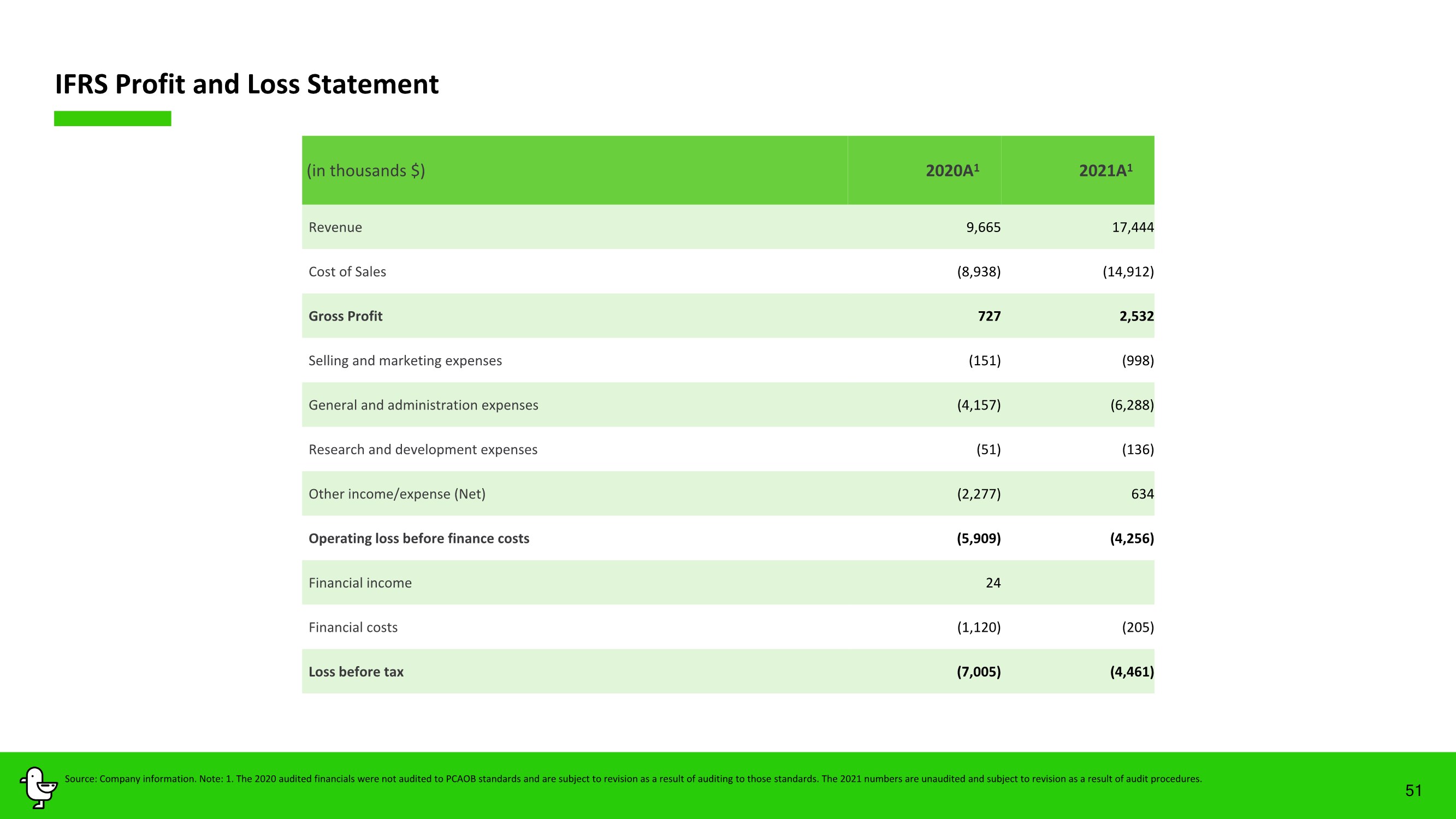

| IFRS Profit and Loss Statement (in thousands $) 2020A1 2021A1 Revenue 9,665 17,444 Cost of Sales (8,938) (14,912) Gross Profit 727 2,532 Selling and marketing expenses (151) (998) General and administration expenses (4,157) (6,288) Research and development expenses (51) (136) Other income/expense (Net) (2,277) 634 Operating loss before finance costs (5,909) (4,256) Financial income 24 Financial costs (1,120) (205) Loss before tax (7,005) (4,461) 51 Source: Company information. Note: 1. The 2020 audited financials were not audited to PCAOB standards and are subject to revision as a result of auditing to those standards. The 2021 numbers are unaudited and subject to revision as a result of audit procedures. |

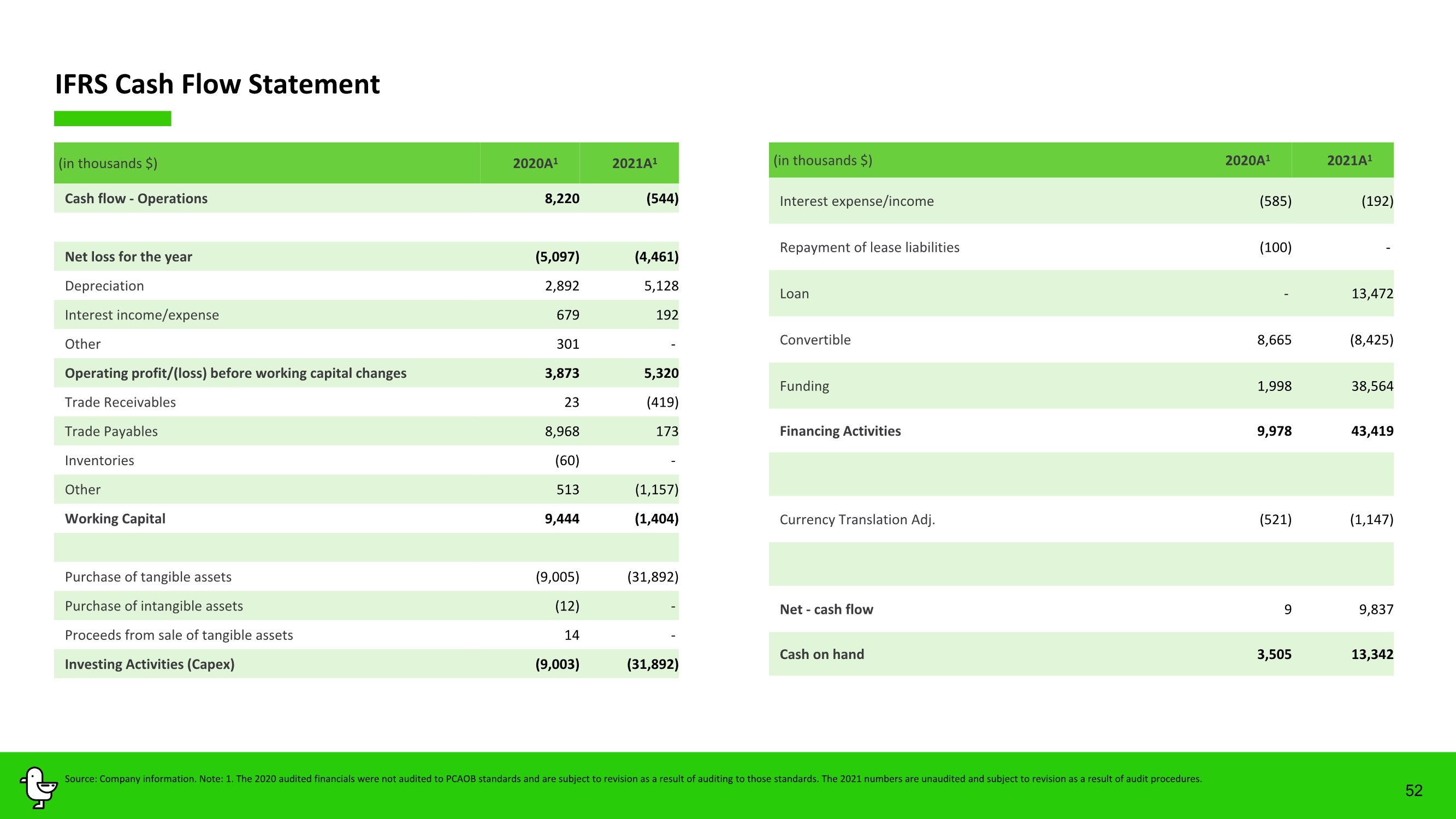

| 52 IFRS Cash Flow Statement (in thousands $) 2020A1 2021A1 Cash flow - Operations 8,220 (544) Net loss for the year (5,097) (4,461) Depreciation 2,892 5,128 Interest income/expense 679 192 Other 301 - Operating profit/(loss) before working capital changes 3,873 5,320 Trade Receivables 23 (419) Trade Payables 8,968 173 Inventories (60) - Other 513 (1,157) Working Capital 9,444 (1,404) Purchase of tangible assets (9,005) (31,892) Purchase of intangible assets (12) - Proceeds from sale of tangible assets 14 - Investing Activities (Capex) (9,003) (31,892) (in thousands $) 2020A1 2021A1 Interest expense/income (585) (192) Repayment of lease liabilities (100) - Loan - 13,472 Convertible 8,665 (8,425) Funding 1,998 38,564 Financing Activities 9,978 43,419 Currency Translation Adj. (521) (1,147) Net - cash flow 9 9,837 Cash on hand 3,505 13,342 Source: Company information. Note: 1. The 2020 audited financials were not audited to PCAOB standards and are subject to revision as a result of auditing to those standards. The 2021 numbers are unaudited and subject to revision as a result of audit procedures. |

| 53 Risk Factors Risks Related to Marti’s Business and Industry • We have a relatively short operating history and a new and evolving business model, which makes it difficult to evaluate our future prospects, forecast financial results and assess the risks and challenges we may face. • We have incurred operating losses in the past and may not be able to achieve or maintain profitability in the future. • If we fail to retain existing riders or add new riders, or if our riders decrease their level of engagement with our products and services, our business, financial condition and results of operations may be significantly harmed. • We operate in a new and rapidly changing industry, which makes it difficult to evaluate our business and prospects. • If we fail to properly manage our anticipated growth, our business could suffer. • We intend to expand our business and may enter into new lines of business or geographic markets, which may result in additional risks, uncertainties and costs in our business. • We may acquire other businesses, which could require significant management attention, disrupt our business, dilute stockholder value, and adversely affect our operating results. • We will need additional capital, and we cannot be certain that additional financing will be available. • Poor weather adversely affects the use of our services, which causes seasonality in our business and could negatively impact our financial performance from period to period. • Future operating results depend upon our ability to obtain vehicles that meet our quality specifications in sufficient quantities on commercially reasonable terms. • We rely on third-party insurance policies to insure us against certain operations-related risks. If our insurance coverage is insufficient for the needs of our business or our premiums or deductibles become prohibitively expensive or if our insurance providers are unable to meet their obligations, we may not be able to mitigate the risks facing our business, which could adversely affect our business, financial condition and results of operations. • We do not maintain insurance policies for certain risks related to loss or damage to our vehicles, and increases in vandalism or theft could adversely affect our business, financial condition and results of operations. • Illegal, improper, or inappropriate activity of riders could expose us to liability and harm our business, brand, financial condition, and results of operations. • Exposure to product liability in the event of significant vehicle damage or reliability issues could harm our business, financial condition, and results of operations. • Our metrics and estimates, including the key metrics included in this Investor Presentation, are subject to inherent challenges in measurement, and real or perceived inaccuracies in those metrics may harm our reputation and negatively affect our business. • We rely on third-party payment processors to process payments made by users on our software platform, and if we cannot manage our relationships with such third parties and other payment-related risks, our business, financial condition, and results of operations could be adversely affected. • We may in the future rely on third parties to provide services to us, and if we cannot obtain third party services our business, financial condition, and results of operations could be adversely affected. • The markets in which we operate are highly competitive, and competition represents an ongoing threat to the growth and success of our business. • If our vehicles, mobile applications, or other services have defects, the reputation and brand of our products and services could suffer, which could negatively impact the use of our products and services, and negatively impact our operating results and financial condition. • Our company culture has contributed to our success and if we cannot maintain this culture as we grow, our business could be harmed. • If we are unable to attract, hire and retain key employees and qualified personnel, our ability to compete may be harmed. • We are subject to risks associated with doing business in an emerging market. • Our headquarters and other operations and facilities are located in Turkey and, therefore, our prospects, business, financial condition and results of operations may be adversely affected by political or economic instability in Turkey. • Turkey’s economy is subject to inflation and risks related to its current account deficit. • Foreign exchange rate risks could affect the Turkish macroeconomic environment, could affect your investment and could significantly affect our results of operation and financial position in future periods if hedging tools are not available at commercially reasonable terms. • Turkey is subject to internal and external unrest and the threat of future terrorist acts, which may adversely affect us. • Conflict and uncertainty in neighboring and nearby countries may have a material adverse effect on our business, financial condition, results of operations or prospects. • Turkey’s economy has been undergoing a significant transformation and remains subject to ongoing structural and macroeconomic risks. Risks Related to Marti’s Intellectual Property and Technology • Our user growth and engagement on mobile devices depend upon effective operation with mobile operating systems, networks, and standards that we do not control. • Our business could be adversely impacted by changes in the Internet and mobile device accessibility of users and unfavorable changes in or our failure to comply with existing or future laws governing the Internet and mobile devices. |

| 54 Risk Factors • We rely on third parties maintaining open marketplaces to distribute our application and provide the software we use in certain of our products and offerings. If such third parties interfere with the distribution of our products or offerings or with our use of such software, if we are unable to maintain a good relationship, or if marketplaces are unavailable for any prolonged period of time, our business will suffer. • The operators of digital storefronts on which we publish our mobile application in many cases have the unilateral ability to change and interpret the terms of our contract with them. • We may be parties to intellectual property rights claims and other litigation that are expensive to support, and if resolved adversely, could have a significant impact on us and our stockholders. • If we are unable to protect our intellectual property, the value of our brand and other intangible assets may be diminished, and our business may be adversely affected. • Any significant disruption in our services or in our information technology systems could result in a loss of users or harm our business. • Damage to, or failure of, our systems or interruptions or delays in service from our third-party cloud service platforms could impair the delivery of our service and harm our business. • Our service relies on GPS and other Global Satellite Navigation Systems (“GNSS”). • Computer malware, viruses, hacking, and phishing attacks, and spamming could harm our business and results of operations. • Systems failures and resulting interruptions in the availability of our website, applications, platform, or offerings could adversely affect our business, financial condition, and results of operations. Risks Related to Laws and Regulations • Action by governmental authorities to restrict access to our products and services in their localities could substantially harm our business and financial results. • Our business is subject to regulation by multiple governmental authorities, and our inability to maintain existing governmental approvals or to obtain governmental approvals in the future could adversely impact our financial results or operations. • Government regulation of the Internet and user privacy is evolving and negative changes could substantially harm our business and operating results. • Internet and e-commerce regulation in Turkey is recent and is subject to further development. • We collect, store, process and use personal information and other customer data, which subjects us to governmental regulation and other legal obligations related to privacy, information security, and data protection, and our actual or perceived failure to comply with such obligations could harm our business. • Expansion of products or services could subject us to additional laws and regulations, and any actual or perceived failure by us to comply with such laws and regulations or manage the increased costs associated with such laws or regulations could adversely affect our business, financial condition, or results of operations. • We are regularly subject to claims, lawsuits, government investigations, and other proceedings that may adversely affect our business, financial condition, and results of operations. • We may face lawsuits from local governmental entities, municipalities, and private citizens related to the conduct of our business. • We are subject to various existing and future environmental health and safety laws and regulations that could result in increased compliance costs or additional operating costs and restrictions. Failure to comply with such laws and regulations may result in substantial fines or other limitations that could adversely impact our financial results or operations. • We may be subject to tax audits that may result in additional tax liabilities. • We may be exposed to changes in tax laws and regulations as well as their interpretation and implementation. • Our operating plan requires us to source parts, materials and supplies internationally, and supply chain disruptions, foreign currency exchange rate fluctuations and changes to international trade agreements, tariffs, import and excise duties, taxes or other governmental rules and regulations could adversely affect our business, financial condition, results of operations and prospects. • We may be subject to administrative fines and our reputation may be harmed if the Turkish Competition Authority were to determine that we did not comply with Turkish competition laws and regulations. • We are exposed to the risk of inadvertently violating anti-corruption, anti-money laundering, anti-terrorist financing and economic sanctions laws and regulations and other similar laws and regulations. • Because we are incorporated under the laws of the Cayman Islands, and Marti’s management and operations are based in Turkey, you may face difficulties in protecting your interests, and your ability to protect your rights through the U.S federal courts may be limited. Risks Related to Marti’s Financial Results • Our ability to utilize historic losses to offset income in future years may be limited, including as a result of significant changes in our shareholder base or as a result of acquisition activity. • We are exposed to fluctuations in currency exchange rates. • Unanticipated changes in our income tax rates or exposure to additional tax liabilities may affect our future financial results. • We are subject to tax in multiple jurisdictions, and changes in tax laws (or in the interpretations thereof) in the United States, Turkey or in other jurisdictions could have an adverse effect on us. • We establish tax provisions, where appropriate, on the basis of amounts expected to be paid to (and recovered from) tax authorities and, as a result, changes in tax laws (or in the interpretations thereof) could have an adverse effect on us. |

| 55 Risk Factors Risks Related to the Business Combination • The NASDAQ or NYSE may not continue to list Galata or Company securities, which could limit investors' ability to make transactions in our securities and subject us to additional trading restrictions. • Because the post-combination company will become a publicly-traded company by virtue of a merger as opposed to an underwritten initial public offering, the process does not use the services of one or more underwriters, which could result in less diligence being conducted. • Past performance by Galata’s sponsor or its affiliates, or the directors and officers of Galata, may not be indicative of future performance of an investment in Galata or the post-combination company. • If third parties bring claims against Galata, the proceeds held in the trust account could be reduced. In such event, Galata directors may decide not to enforce the indemnification obligation of Galata’s sponsor, resulting in a reduction in the amount of funds in the trust account available for distribution to public stockholders. • If Galata is unable to complete an initial business combination by July 8, 2023, they will cease all operations except for the purpose of winding up, redeeming 100% of the outstanding public shares and, subject to the approval of its remaining stockholders and the Galata Board, dissolving and liquidating. In such event, third parties may bring claims against Galata and, as a result, the proceeds held in the trust account could be reduced. • Galata stockholders may be held liable for claims by third parties against Galata to the extent of distributions received by them. • Activities taken by existing Galata stockholders to increase the likelihood of approval of the Business Combination proposal and the other proposals described in the proxy statement that will be filed in connection with the Business Combination could have a depressive effect on our stock. • Galata stockholders will experience dilution as a consequence of, among other transactions, the issuance of common stock as consideration in the Business Combination and the private placement investment. Having a minority share position may reduce the influence that Galata’s current stockholders have on the management of Galata. • The Company and Galata expect to incur significant transaction costs in connection with the Business Combination. Whether or not the Business Combination is completed, the incurrence of these costs will reduce the amount of cash available to be used for other corporate purposes by Galata if the Business Combination is not completed. • The Company's operating and financial results forecasts, which were presented to the Galata Board, may not prove accurate. • Upon executing a definitive agreement with respect to the Business Combination between the Company and Galata, Galata will be prohibited from entering into certain transactions that might otherwise be beneficial to it or its stockholders. • Galata or the Company may issue additional equity securities without your approval, which would dilute your ownership interests and may depress the market price of Galata’s common shares. • Galata and/or the Company may seek additional financing prior to completion of the Business Combination or otherwise provide incentives to investors to approve consummation of the Business Combination, which may dilute your ownership interests and may depress the market price of Galata’s common shares. • Galata and the Company may require additional financing prior to completion of the Business Combination in order to satisfy the conditions to consummation of the Business Combination, which additional financing may not be able to be obtained. Risks Related to the Post Combination Company Following the Business Combination • Galata may redeem the public warrants prior to their exercise or expiration at a time that is disadvantageous to public warrant holders, thereby making their pubIic warrants worthless, and exercise of a significant number of the public warrants could adversely affect the market price of common stock. • Galata and the Company’s ability to successfully effect the Business Combination and to be successful thereafter will be dependent upon the efforts of certain key personnel, including the key personnel of the Company. The loss of key personnel could negatively impact the operations and profitability of the post-combination business and its financial condition could suffer as a result. • The post-combination company's management team will have limited experience managing a public company. • The requirements of being a public company may strain the post-combination company's resources and distract its management, which could make it difficult to manage its business. Particularly after the Company is no longer an emerging growth company," • Unanticipated changes in effective tax rates or adverse outcomes resulting from examination of the Company’s income or other tax returns could adversely affect the Company’s financial condition and results of operations. • Subsequent to the completion of the Business Combination, the Company may be required to take write-downs or write-offs, restructuring and impairment or other charges that could have a significant negative effect on the Company’s financial condition, results of operations and stock price, which could cause you to lose some or all of your investment. • Following the consummation of the Business Combination, our only significant asset will be our ownership interest in the Company business and such ownership may not be sufficiently profitable or valuable to enable us to pay any dividends on common stock or satisfy our other financial obligations. • If the Business Combination's benefits do not meet the expectations of investors, stockholders or financial analysts, the market price of our securities may decline. • Pursuant to the Dodd-Frank Act and SEC rules, the post-combination company will be required to file public disclosures regarding the country of origin of certain supplies, which could damage our reputation or impact our ability to obtain merchandise if customers or other stakeholders react negatively to our disclosures. • As a private company, we have not been required to document and test our internal controls over financial reporting nor has management been required to certify the effectiveness of our internal controls and our auditors have not been required to opine on the effectiveness of our internal control over financial reporting. As such, we may identify material weaknesses in our internal control over financial reporting that could lead to errors in the post-combination company's financial reporting, which could adversely affect the post-combination company's business and the market price of our securities. • The post-combination company will be a holding company and depend upon its subsidiaries for its cash flows. |

| LET’S RIDE! |